With two-thirds of calendar year 2019 now in the books, we would like to do a quick review of the energy markets for this time frame and examine the drivers for the remainder of the year and beyond regarding energy pricing in the Midwest. Energy prices have really been on a slow grind lower in 2019 year-to date.

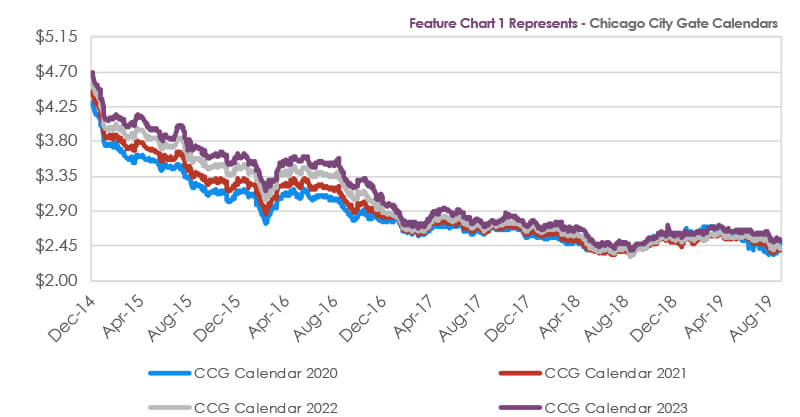

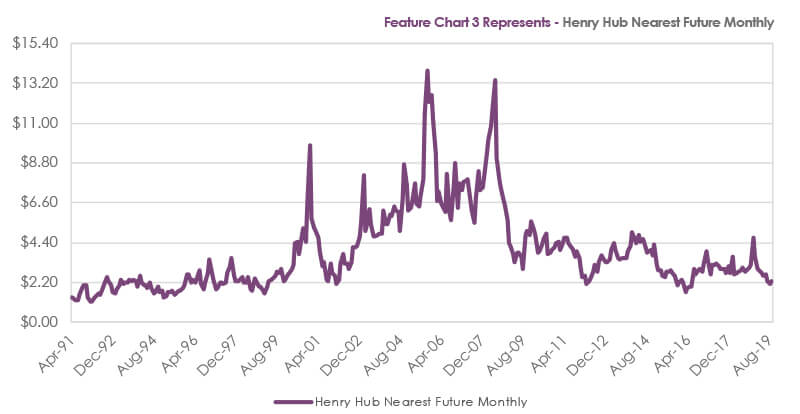

Natural gas prices started the year at elevated levels as a result of a strong 2018 year-end rally based on tight supplies and very cold November 2018 weather. Since then, it has been a steady grind lower with natural gas prices in the Midwest down as the market met higher prices with record supply. In addition, sharply lower Liquefied Natural Gas (LNG) prices have, to some extent, reduced demand. The monthly natural gas cash indices (the indices that set the monthly rate for customers who receive floating rate gas) have been settling lower almost every month YTD. The average monthly settlement for Henry Hub NYMEX has been $2.667 per MMBtu, 13.4% lower than the 2018 average of $3.08 per MMBtu. The NGI Chicago City Gate monthly average has also been lower, averaging $2.544 per MMBtu YTD, 16.32% lower than the 2018 average of $3.041 per MMBTU. Natural gas forward prices have also declined YTD. For the first eight months of the year, The Henry Hub 2020, 2021, 2022 and 2023 calendar strips have declined 9.85%, 5.84%, 5.70%, and 4.76% respectively to $2.40, $2.45, $2.50 and $2.58 per MMBtu. The Chicago City Gate 2020, 2021, 2022 and 2023 calendar strips have fallen 7.86%, 4.06%, 4.36% and 3.34% respectively to $2.35, $2.39, $2.43 and $2.52 per MMBtu. One key takeaway from the market movements is that over the last eight months and even more so since August 2018 the forward curves have shifted from being mostly in backwardation (prices decreasing further out the curve) to a formation of contango (prices increasing further out the curve). The forward curve shape combined with relative price levels have a big influence on whether we recommend to our customers that they fix or float their prices and for what time frame. At this juncture, we still have a bias towards fixing prices for up to three years given the low relative price level and small price contango. Our view could easily change if the price levels and/or shapes of the forward curve change.

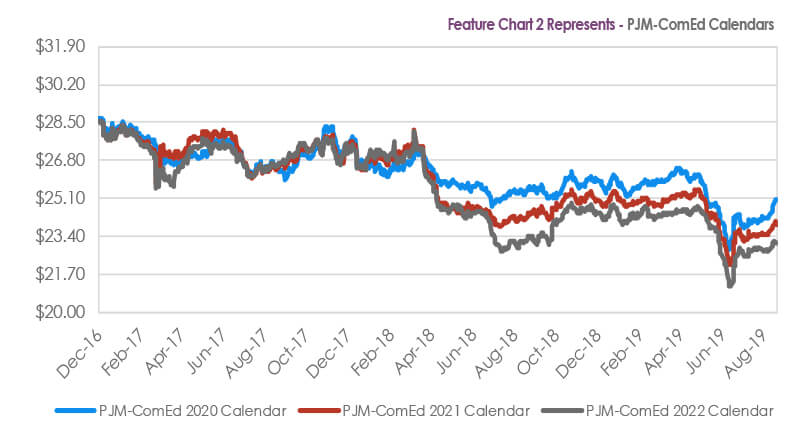

The Midwest power market has also been characterized by lower prices. A surprising development has been the very low day-ahead prices we have observed in 2019. The PJM/ComEd day-ahead average price for the first eight months has been $24.37 per MWh, 15.23% lower than the $28.75 per MWh price seen in 2018. If the full 2019 day-ahead average price finishes below the 2016 price of $26.15 per MWh, it will be the lowest yearly average day-ahead price since ComEd joined the PJM pool in 2006. These low spot prices have pressured the forward prices lower. The 2020, 2021, 2022, and 2023 calendar strips have dropped 4.85%, 4.61%, 5.47%, and 6.35%, respectively, to $24.01, $23.65, $22.87, and $22.64 per MWh. These are very low forward prices and the lowest experienced since ComEd joined PJM. Unlike the natural gas forward curves, the PJM/ComEd forward curves are still characterized by backwardation.

For this reason, we continue to recommend that customers lock in prices far out the price curve. For example, the 2023 price of $22.64 per MWh is 7% below the aforementioned record low day-ahead price of $24.37 per MWh seen January-August 2019. While we know markets can always go lower, we prefer to buy at a discount to spot prices rather than paying a premium in a commodity market that historically has some of the highest upside price volatility (see article on ERCOT).

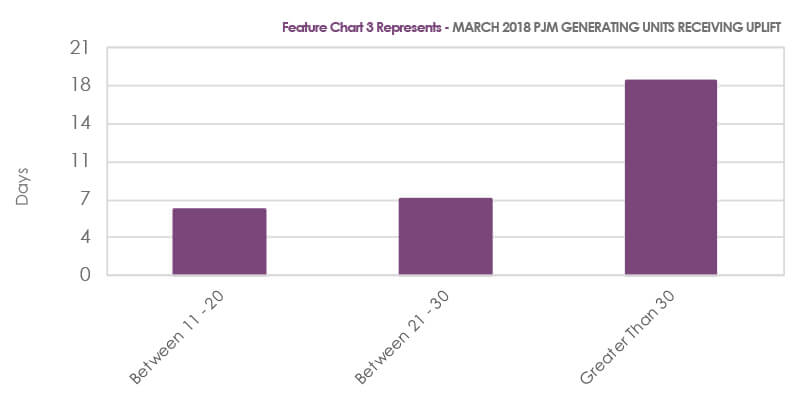

Nuclear and renewable electricity generation subsidies have created problems in the energy market for PJM, causing prices to clear at lower prices than they would normally. The PJM market is an electricity auction market and the goal is to allocate generation resources in the most efficient manner. With the introduction of units that are subsidized, some of the units offer themselves into the pool at lower prices then they normally would. Further, with many of the renewable resources being intermittent, some units are often called to run in what is called out of merit and paid uplift. These generators are not paid the clearing price at the time but a price that covers all of their costs. The argument to do this is that it improves pool performance, but many other generators feel as though they are not being compensated fairly as the clearing price stays artificially low.

This leads us to expand on our thoughts for the remainder of the year and next year. The Midwest energy markets from a price perspective are at very attractive levels. While we have been at low levels for the last several years, the markets are about as cheap as they have ever been. In other monthly reports we have highlighted some of the elements driving prices lower. A list of the reasons includes but is not limited to:

- cheap natural gas from horizontal fracturing

- the addition of many subsidized, zero-cost fuel renewable electricity generating facilities

- PJM dispatch regulations

- nuclear electricity generation subsidies

- energy efficiency measures

- natural gas pipeline expansions

- rapid increases in the deployment of battery storage as a grid tool

None of these are new but two that stand out this year are nuclear electricity generation subsidies as they have expanded to more states (Ohio and New Jersey) in PJM and the rapid increase in battery storage attached to subsidized solar projects. It is our opinion that these two items have caused the market to overshoot to the downside. These are real issues that are bearish from a price point, particularly electricity. However, we think that storage will take some time to develop and that both the nuclear and renewable energy subsidies could come under attack as they are financed out of state budgets that can be changed. Further, although not yet implemented, PJM is looking at options to raise the clearing price for all generators as it has been proven that the state subsidies do distort the auction process. Regarding natural gas, we believe the switch to a market structure of contango is indicating that price may have reached a bottom and we still see natural gas as the global transition fuel over the next ten years. For these reasons, we think commercial customers should lock in fixed prices for their energy obligations as opposed to being lured into trying to capture 5-10% potential gains from lower floating prices. In other words, it is like trying to pick up pennies in front of a steamroller. You can do it for a while, but eventually you are going to get rolled. Again, this is particularly true in event-driven energy markets.

Analyst – David Mousseau

Source – PJM, CME, Utility Dive, PJM Market Monitor