As we move into the last third of the year, we would like to do a quick review and forecast of the energy markets for the Midwest.

The first two months of the year saw a continued trend lower for both natural gas and electricity prices as the entire country experienced one of the warmest winters on record. The situation was exacerbated by the fact we entered the winter with record levels of natural gas in storage. As is typical in commodity markets, just when the situation looked dire, prices turned on a dime and both electricity and natural gas made significant lows during between the end of February and the middle of March depending on the market and term (quite important) being evaluated. Front-month Henry Hub natural gas futures put in a 17-year low on March 3rd at $1.64 Per MMBtu while 12-month forward PJM/ComEd electricity bottomed at $25.42 per MWh on March 8th.

It is important to note that futures and forwards (particularly for natural gas) rebounded much quicker than their corresponding spot or cash prices. Futures and forwards prices are expectations of future spot and cash prices and for a period of time, there was a true disconnect between cash/spot and longer-dated futures/forwards. Spot prices for Chicago City Gate gas essentially remained below $2.00 MMBTU until May 27th while the 12-month CCG forward was trading at $2.77. The spot prices quickly caught up to the forwards in the first two weeks of June as hot weather (increasing demand for natural-gas-fired electricity generation) and the continuing trend of lower natural gas storage injection numbers forced spot prices higher. After making its aforementioned low, the PJM/ComEd 12-month rolling forward grinded 18.57% higher to print a yearly high of $30.14 on June 28th. We then spent July and August in a very narrow $2.00 per MWh range despite the very warm summer and the 12-month rolling forward closed on August 31st at $28.97 per MWh.

An important question now is, where do these markets go from here? While impossible to know, it is useful to review some of the things we do know. For the PJM/ComEd area, we do know that we did not experience any scarcity hourly pricing this summer despite some of the higher loads experienced in the last few years and very warm weather across the PJM territory. The prices in other parts of PJM did go higher but still short of real scarcity pricing. We know that even 10-20 hours of +$500.00 prices can influence future forward prices, and that did not occur. We know that demand-side management peak shaving techniques have impeded load growth. Countering these bearish items is the fact that the State of Illinois could still lose 7,000 MWs of generating capacity (see last month’s article) in the next couple of years due to plant retirements. We also know that the forward market is a discounting mechanism and these items are known to the market.

We also know that given the continued growth of natural gas generation that natural gas pricing is very important to the electricity baseload market pricing and this may hold the key to future pricing. While the natural gas market has benefited from low prices due to the fracturing phenomenon, the impact may start to subside due to the building of pipelines that will allow for the moving of natural gas from the large shale areas (Marcellus and Utica Shales in Ohio and Pennsylvania) to areas where it can be used for manufacturing and exported as Liquefied Natural Gas (LNG). It is quite likely that natural gas consumption is going to continue to grow globally as it is a bridge fuel away from petroleum and it is clear that the political pressures around climate change are going to demand a fuel that is somewhat more environmentally friendly, though natural gas is still a fossil fuel. One large change slowly evolving is the change in contract pricing in LNG from a link to oil pricing to one based on USA natural gas prices. This is reasonably bullish long-term in our opinion, and we think that provides support to both natural gas and electricity prices over the next few years.

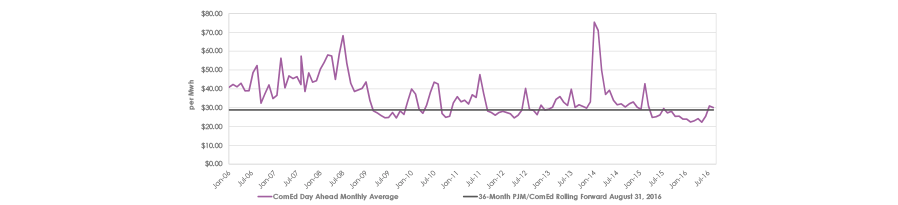

Finally, what we do know for sure from the data we have is that both electricity and natural gas are still pretty cheap from a historical perspective (see charts) and without a great deal of risk premium built into forward prices. We continue to advise that most customers (depending on their load profiles) should lock half to 100% of their obligations for both commodities depending on their profile for as long as three years. We will continue to monitor the markets and will review our forecasts as more information reveals itself.

Analyst – David Mousseau

Information Sources Energy Information Administration (EIA), CME, and CONSTELLATION ENERGY