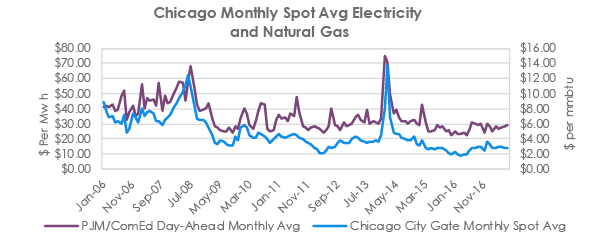

This proliferation of renewable generation has been fueled by production tax credits, which have been as high as $23.00 per MWh. Since the fuel cost for these resources is zero, there have been many instances of negative pricing over the last several years (less in the last year) during periods of low demand (generally at night). An examination of Chart 1 shows the steady collapse in the average daily price of both natural gas and electricity over the last nine years (except for the Polar Vortex).

The central premise of the PJM report entitled “Energy Price Formation and Valuing Flexibility” is that power prices are generally too low, and that is a result of the market structure. As customers know all too well, though we have seen a noticeable decline in spot and forward power prices, the overall retail energy price has not dropped as much because capacity prices have increased, as Chart 2 indicates. This is in addition to other charges (both on the commodity and distribution side of their invoices) that have been added. The relationship between capacity prices and wholesale prices is important because generators of electricity are paid for both. With the low wholesale prices of the last few years, generators have tended to be paid more for capacity, somewhat offsetting lower energy-only revenues.