One other important reason we believe customers should lock in the actual energy portion of their utility obligation is that non-commodity costs continue to rise rapidly. Demand Response (being paid for reducing demand during times of system stress) is an avenue to offset rising non-commodity costs, but not all customers are large enough or have the flexibility to participate. Similarly, a customer could initiate energy efficiency projects that would reduce demand, but these usually require an upfront cost. However, the lowest hanging fruit right now is locking in the low discounted energy prices.

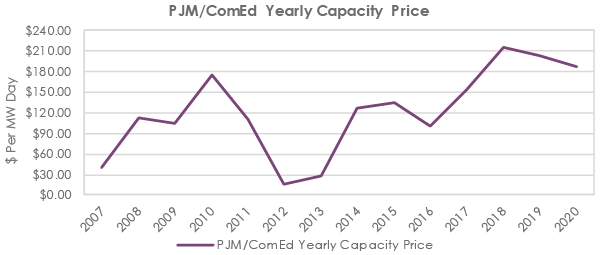

In our feature articles, we have occasionally spoken about regulatory risk. There was the PJM capacity performance implementation that resulted in higher capacity costs (see chart 3) for customers. This year has seen the implementation of the Zero Emission Credits (ZECS) in both Illinois and New York, which created higher customer costs via a regulatory mechanism. This is in addition to the seemingly yearly continued hikes seen in distributions charges by both natural gas and electric utilities. Oddly, many of these charges have been driven by the low energy costs, flat demand and behind the meter distributed generation. Utilities are seeing their revenues flatten while the cost of improving an ageing infrastructure continues to increase. We see this trend continuing, adding to our view that lower electricity prices can offset some of these increases.