With two-thirds of calendar year 2018 now completed, here is a quick review of the energy markets in the Midwest. The markets continue to be marked by a lack of volatility, but there are always changes occurring. We will attempt to highlight these changes and make some forecasts for the last third of the year.

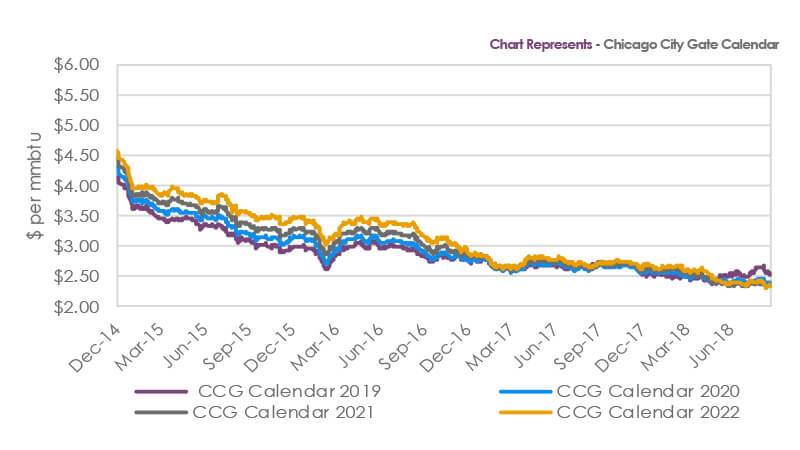

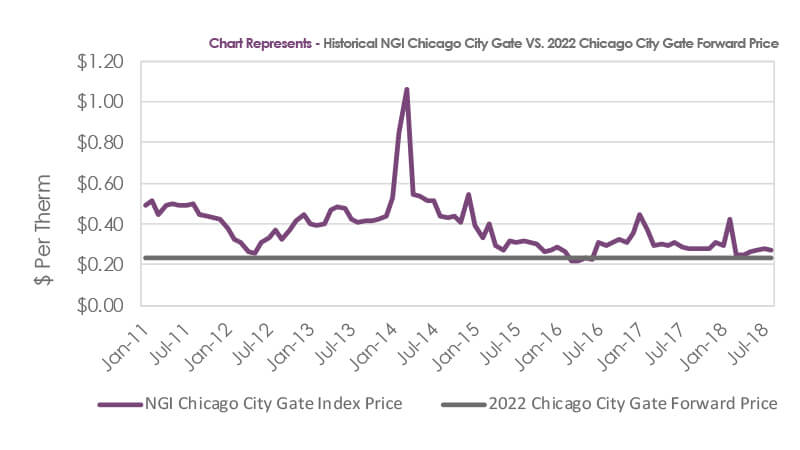

The natural gas markets have been quiet in terms of volatility, and there has been a disconnect developing between the spot markets and the further-dated forwards and futures. The monthly cash indices (the index that sets the rate for most customers who receive floating rate gas) of NYMEX prompt and NGI Chicago City Gate have settled each month without much fanfare. The average monthly NYMEX settlement for the first eight months of the year has been $2.90 per MMBtu, and the NGI Chicago City Gate average comes in at $2.87 per MMBtu. As a reference point, the 2017 Henry Hub average was $3.20 per MMBtu and the 2017 NGI Chicago City Gate average was $3.11 per MMBtu. The more important developments have been in the further-dated curves where further price backwardation has been built into the forward curves. In the first eight months, the Henry Hub 2019, 2020, 2021, and 2022 calendar strips have declined .95%, 6.40%, 9.94%, and 11.15%, respectively, to $2.79, $2.64, $2.57, and $2.56 per MMBtu. The Chicago City Gate 2019, 2020, 2021, and 2022 calendar strips have fallen .42%, 7.55%, 11.13%, and 12.813%, respectively, to $2.59, $2.42, $2.36, and $2.36 per MMBtu.

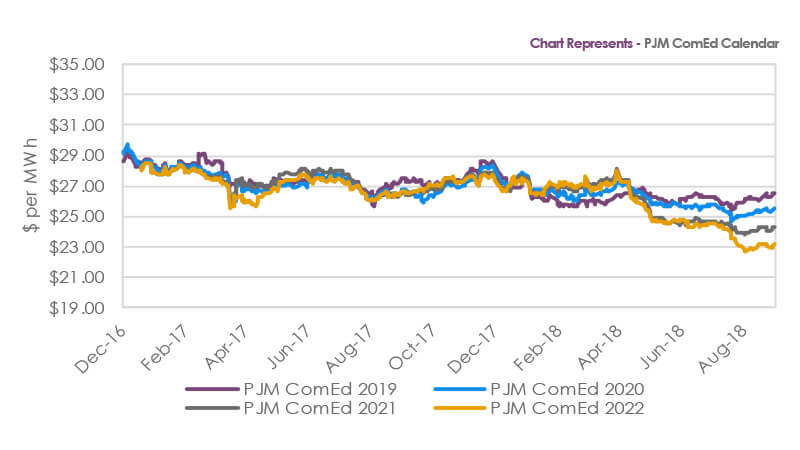

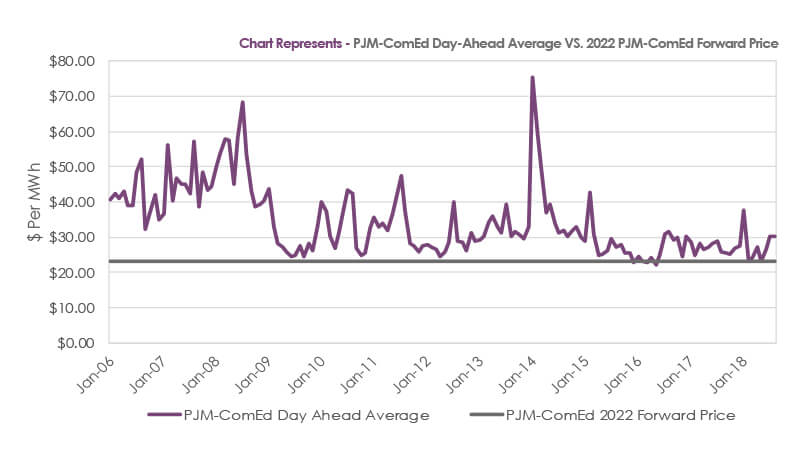

The power market has also been quiet. The PJM/ComEd Monthly Day-ahead average for the first eight months has been $27.86 per MWh, an increase of 3.41% over the 2017 average price. However, like natural gas, the further-dated PJM/ComEd power curves have moved to greater backwardation in the first eight months of the year. The PJM/ComEd 2019, 2020, 2021, and 2022 forward calendar strips have declined 4.22%, 8.43%, 11.70%, and 15.10%, respectively, to $26.53, $25.49, $24.29, and $23.23 per MWh.

To summarize, energy prices have been somewhat steady in the front of both the power and natural gas curves but noticeably weak in the back end of the curves. We have noticed that the further-dated Chicago City Gate-Henry Hub basis is quite weak for the years 2019-2022, with Chicago City Gate trading at an approximate 20 cent per MMBtu discount to Henry Hub for these years when the current cash basis is discounted by 3 cents. We have also noticed that the prices for 2020-2022 in ComEd are at significant discounts to the Day-ahead average price (the price the forward price is predicting) observed in the last three years.

In past articles, we have spoken about some of the reasons for the low prices for both electricity and natural gas that have been observed in the last few years. A list of the reasons includes, but is not limited to:

- cheap natural gas from horizontal fracturing

- the addition of many subsidized, zero-cost fuel renewable electricity generating facilities

- PJM dispatch regulations

- nuclear electricity generation subsidies

- energy efficiency measures

- natural gas pipeline expansions

These are all valid reasons for low prices, but we do believe that these are known factors. Our job as risk managers is to manage our clients’ risk and provide information on the unknown factors that will affect future pricing. There are a handful of items we believe are not being adequately factored into forward pricing:

- Demand growth factors for both power and natural gas are underestimated.

- The market is not pricing in any risk of fracking being curtailed or stopped due to environmental considerations.

- While we do believe in the emergence of utility-scale electricity storage, we think the price curves will need to be higher to produce large-scale implementation.

- As demonstrated in the NYISO proposal, if a social cost of carbon is introduced as an added component in wholesale electric prices that will cause a significant increase in that pricing. Even a small probability of that outcome is not being included as a risk factor.

- The market may be underestimating load growth and overestimating the impact of further energy efficiency projects.

What is an absolute truth is that nobody knows for certain where prices are going. We do know some energy price history, and we are aware that technological change can at times make history less relevant. That said, we continue to encourage our customers to lock down a majority position of their energy exposure out to four years. The most influential reason for this recommendation is that the forward prices in 2021-22 are trading at discounts up to 19% to the 2018 cash price in Chicago City Gate for natural gas. In the PJM/ComEd electricity market, the discount for the 2021-22 forward to the 2018 monthly day-ahead average price is about 15%. At some point, the forward price and spot price will converge. Whatever the result, the customer who buys forward today is starting with a double-digit % lead.

Analyst – David Mousseau

Source – CME Group, PJM, Reuters