The ongoing relationship/concept between spot and forward prices is an important one to understand for customers when it comes to the timing of locking in electricity and natural gas contracts. We have used the Chicago market as an example since we have many customers here, but would caution our growing customer base in other areas of the country to review the specific relationships in their area since the conditions in one area of the country can be quite different than in another.

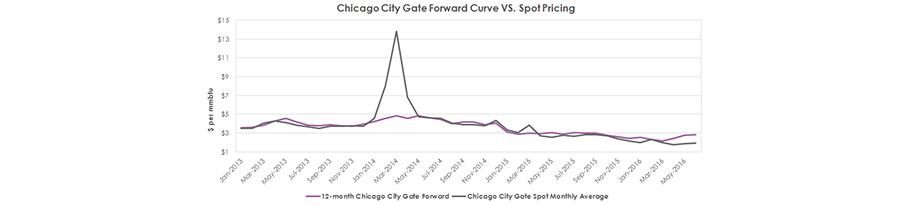

The first concept worth highlighting is that forward prices (in these cases, 12-month rolling forwards) in both charts are less volatile and that in general over long periods of time, spot prices exhibit higher volatility. The second point is somewhat counter intuitive in that over long periods of time, spot prices are usually lower (though as charts show, not always) than forward prices. This is true for the basic economic fact that forward prices have an event premium built into that spot prices do not. That said, the Polar Vortex event (and many other events before it) is an example of why that premium exists.

After the long decline (with some weak rallies included) in both spot and forward prices for both commodities since the Polar Vortex, we recently have seen some strength in forward prices while spot prices have remained extremely low. The current premium for forward pricing over current spot pricing in the Chicago natural gas market is as high as it has been in almost 3 years and the current premium in the electricity market is at the high end of the range of outcomes observed since 2011.

Given these facts, it may be appear that the smart strategy for a customer whose current fixed price contract end date is soon is to receive spot pricing and avoid paying the “forward premium”. There are times this may be true but we would caution that this might not be one of those times in either commodity. The primary reason we are counseling clients to lock in a good portion of their price risk in both NG and electricity is that the historically low levels of both spot and forward prices in this region are dictating that it is prudent because any possible downside benefit is outweighed by the upside risk.

Forward prices to a large extent are discounting mechanisms and we see the recent rise in forward prices (with more strength the further we go out) as indicative of the market recognizing that there has been a change in the future supply/demand dynamics in the market, and that we are at possible point in the market where the trend is changing from a bearish standpoint to one where price rises may occur more frequently and with more velocity.

Analyst – David Mousseau

Sources – CME, Reuters