Many of the OPEC members provide very cheap or free oil to their people and as populations increase and affluence extends, a greater proportion of output is required to satisfy domestic need. When I brought this up last year with Mr El Badri, Secretary General, he impressed upon me the sensitivity of the subject while afterwards I was advised that I should never have brought it up anyway!

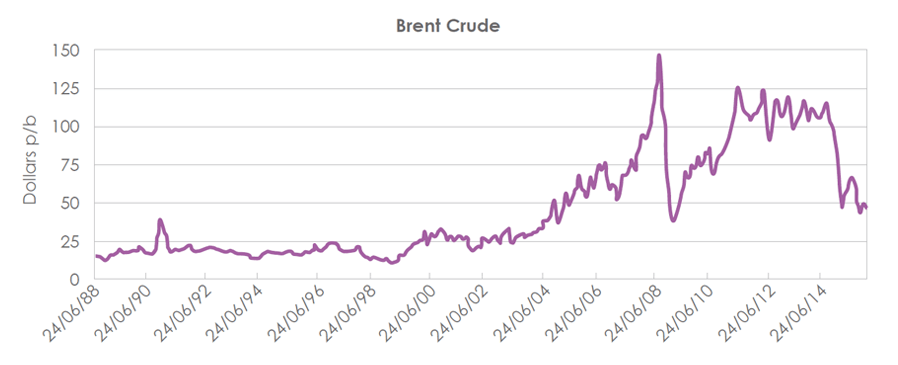

The chart below clearly illustrates the peaks and troughs that have taken place over the last twenty-five years and depending on the circumstance, the peaks have usually corrected themselves.

Before then, in the second half of 1973 when OPEC sold directly to oil companies and accounted for about 80% of internationally traded oil, its power was demonstrated when it imposed a series of unilateral price increases coupled with a reduction in output. The price soared to $11 pb. From 1978 as OPEC increased prices further to around $18 pb in 1979, economic stagnation followed leading to a drastic rationalisation as consumers sought ways of conserving energy through more energy efficient processes.

Later in 1990, at the time the Iraqi invasion of Kuwait over oil rights and the subsequent Gulf War, the spike doubled the price of oil but as soon as a level of peace was restored, it corrected. Fifteen years on, in 2005 the Kuwait Oil Minister admitted to me that, as Kuwait, he would love to have a price of $30! How the market has changed since then.

The spike in 2008 as the price of crude hit $147 and collapsed back again to below $50, was the turning point. Although few in OPEC will admit this, the high price of oil contributed to the financial crisis of 2008, just as it did in earlier years, keeping much of the developed world in or close to recession. But today, with lower prices and the availability of alternative energy sources fuels with a strong focus on energy conservation, consumers can recover without the traditional dependence on OPEC. The cyclical pattern over the years has again necessitated the need for consumers to reappraise their energy requirements and with greater innovations coming to fruition it would seem that OPEC has virtually priced itself out of the market.

Continued lower prices will encourage recovery. The US is performing well although manufacturing output is falling as it is in China where growth is running at 7% supported by greater activity in the service sector while Japan is back in recession. World growth is some way behind at 3% but at least still positive. We look ahead planning against various forecasts but we should also be wary that those who wrongly forecast the oil price at $200 in 2008 are now forecasting $20. This is significant because the price of oil is built into the cost of many products and such direct and indirect costs would not be sustainable.

The market players are committed to making forecasts but some figures are more credible than others!

OPEC has cleared the way for new markets – Energy Conservation & Alternative Energy sources – compelling it to have to compete in a far more efficient world that is not so heavily dependent on revenue for Oil & Gas. COP21, which has taken place this week in Paris, is another by-product of high energy prices. Although we have had previous gatherings of this nature – Kyoto & Rio – this is the one that seems to be more likely to have any long-term impact than any before.