We have written a few times about the PJM capacity markets here in this report.

Over the last few years, the price of capacity in PJM has generally increased, causing our customers’ invoices to sometimes increase even though electricity prices have generally been declining the last five years. In November 2019, a Washington DC-based energy consulting firm, Grid Strategies LLC, released a report entitled “Too Much of the Wrong Thing: The Need for Capacity Market Replacement or Reform”. While a summary of a 40-pagetechnical report that has a specific viewpoint (the capacity market is highly flawed) is a challenge for a report of our type, we are going to accept the challenge because the report discusses issues that are important to the future electricity costs for our customers.

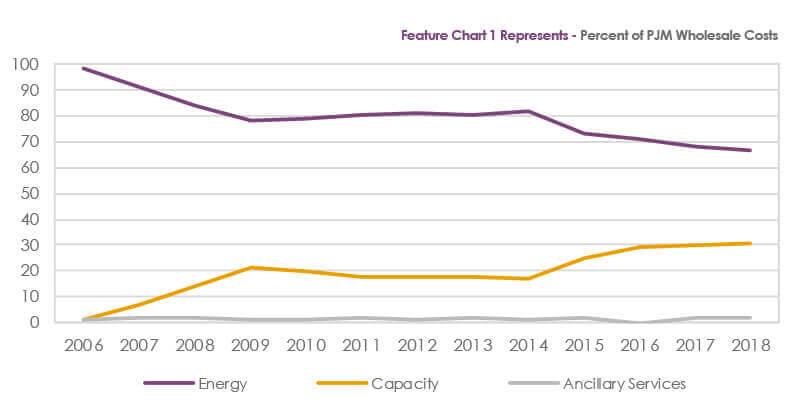

Electricity has the unique quality of being a commodity where supply must meet demand in real-time, and a violation of that tenet can cause the grid to come under extreme stress and cause rolling blackouts. Therefore, all power markets, whether formally organized (PJM, NY-ISO, MISO, etc.) or a single utility control area, maintain a reserve margin of electricity generating capacity above expected peak demand. With the growth of organized auction electricity markets, some capacity markets have become mandatory. In the past few years, the trend in PJM has been towards higher capacity prices (and higher reserve margins) and low energy prices with the net result being that the final wholesale energy cost is comprised of a higher percentage of capacity related costs than electricity costs (see Chart 1). The central argument of the study is that the lower electricity costs observed the last few years have not made up for the generally higher capacity costs paid by customers and that capacity markets are inefficient and not completely competitive. These technical concepts are currently being debated by the Federal Energy Regulatory Commission (FERC) as the scheduled April 2019 PJM capacity auction for the 2022-23 capability period has so far been postponed twice. While we do not want to discuss the complicated aspects of the electricity auction markets in detail, we would like to touch on some issues that could impact customers on a longer-term basis.

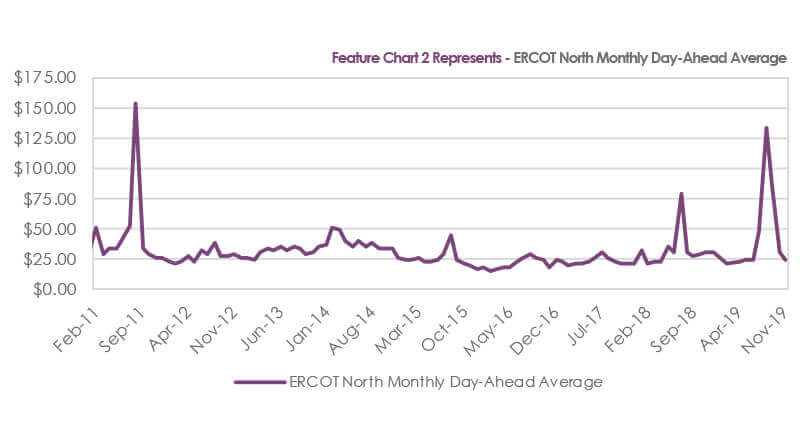

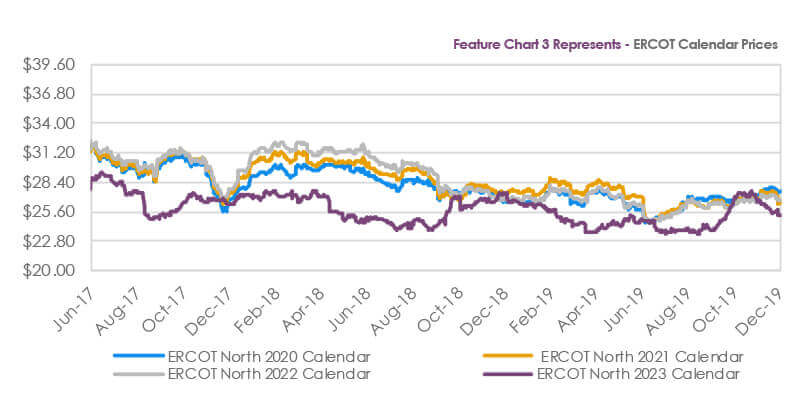

An ongoing debate in the academic area regarding organized electricity markets, both domestically and globally, is whether markets need a capacity market to spur the growth of the generation capability to meet demand. The central idea behind capacity markets is that higher capacity prices will allow electricity generator developers to be able to point to a guaranteed income stream to finance new generation. An opposing view is that an energy-only market (without capacity) will create a scarcity effect to signal when new generation is needed. A concrete and relevant example of the latter is the Electricity Reliability Council of Texas (ERCOT) market, which is energy-only and has a $9000.00 per MWh cap on prices as opposed to the $1000.00 per MWh price cap observed in PJM. We saw some high prices this past summer in ERCOT, and a general review of spot prices against the current ERCOT forward curves (Charts 2 and 3) indicates that the market believes that new generation will be added as the price curve is in distinct backwardation.

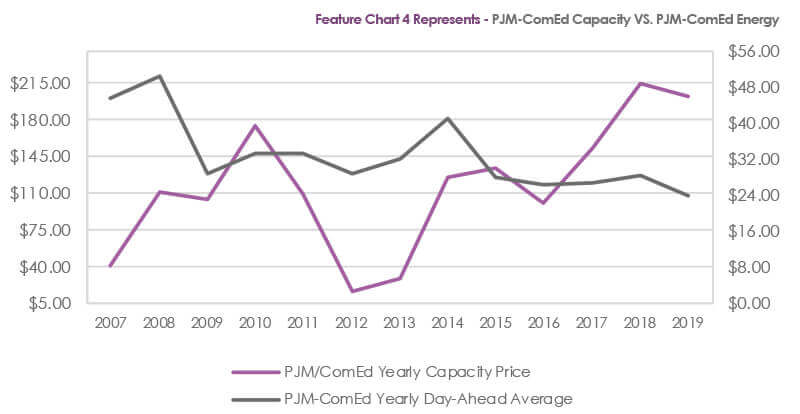

In PJM, we have seen the effect that the higher capacity prices observed in the last five years have resulted in mostly lower electricity prices. This can be seen in Chart 4. Part of the argument occurring around the PJM market discussion is that the low clearing prices (especially this past year) have been unduly influenced by the extreme growth of state-subsidized renewable generation and the subsidies being provided to nuclear electricity generators in three PJM states (Illinois, New Jersey, and Ohio). This is somewhat of a distortion for ComEd and Ameren customers since they pay for the zero emission credits on the distribution portion of their invoice. For calendar year 2019, we have seen extreme pressure on spot prices due not only to lower fuel costs but also the result of generators receiving subsidies and therefore being able to offer their generation to the market at lower prices. There really isn’t a consensus from the PJM stakeholders regarding exactly what to do about the low energy prices and the high capacity prices. A couple of things are clear, though. A sustained period of lower energy prices as observed this year will put financial pressure on all electricity generators, and the pressure to lower capacity prices will also not help. Our opinion of what may happen in the 2022-23 time period is that the PJM market will be one with generally higher energy clearing prices and lower capacity prices.

Analyst – David Mousseau

Source – Reuters, Energy Information Administration (EIA), and Bloomberg