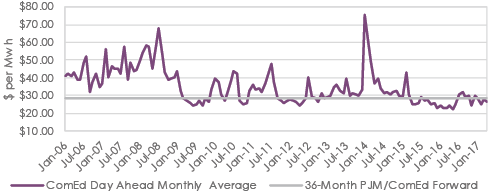

Price VS. PJM/ComEd Monthly Day-Ahead Average

We (Alfa Energy) view ourselves as risk managers, and we do not know exactly where the markets are heading. We do know that we are still very close to the production costs for both commodities, certainly closer in electricity than natural gas. We think the global and domestic demand for natural gas will continue to rise. We believe that improvements to battery storage and demand-side management for electricity will continue but believe they are a longer-term development. We also think that non-commodity costs on consumers’ electricity and natural gas bills will continue to rise in the next few years.

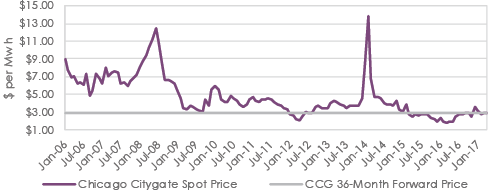

Price vs. Chicago City Gate Monthly Spot Average

The case can be made that both natural gas and electricity may test the relative lows made in February 2017, but we think any move lower will be short-lived and that, if it does happen, the downward movement will be in the front end of the curves, removing some of the current backwardation. While we acknowledge that the energy markets have changed dramatically in the last few years based on technology improvements, we also are students of historical price movements and believe that charts 3 and 4 highlight perfectly that the current upside price risk is higher than any downside reward from potentially lower prices. Energy risk management for procurement is about trying to beat budget numbers, and there are situations where waiting or receiving index pricing could be the correct strategy. However, at current price levels, we believe customers should have at least half of their forward price risk hedged for at least a 24 or 36-month price period considering the current discount for going further out and the relatively low price levels across both the electricity and natural gas complex in the Midwest. We will continue to monitor the market for further developments.

Analyst – David Mousseau

Source – PJM and CME Group