We have now completed two-thirds of the calendar year, so we would like to do a quick review and forecast of the electricity and natural gas markets here in the Midwest.

The quiet conditions that existed in the first third of the year continued in the second third. Electricity and natural gas prices across both price curves traded at reasonably low levels with low relative volatility. From the perspective of a commercial energy consumer, these conditions seem to indicate that this a good time for purchasing energy. This is partially correct and in this article, we will highlight some developments that are adding costs to a customer’s final monthly invoice. Initially, we would like to review the price action of 2017 year-to-date (YTD) and make some projections on pricing for the final third of the year.

One of the characteristics of this market over the first eight months has been the relative weakness of natural gas to electricity, which is reflective of the now very cheap production costs of natural gas versus the fact that electricity prices are trading near their actual production costs. The Chicago City Gate natural gas 12-month forward fell a noticeable 20.27% to $2.89 per MMBtu, the 24-month forward lost 15.87% to $2.81 per MMBtu, and the 36-month forward dropped 12.96% to $2.74 per MMBtu. The PJM/ComEd 12-month forward retreated in value by 6.28% to $28.57 per MWh, the 24-month was off by 6.05% $27.79 per MWh, and the 36-month fell 5.89% to $27.54 per MWh.

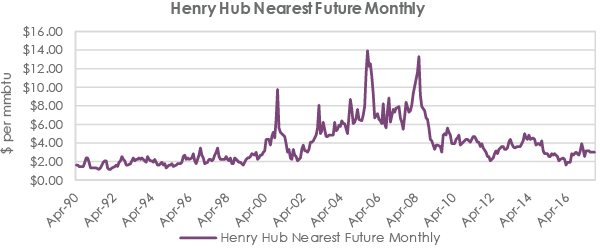

When we step back and try to analyze where the market will go from here, there are many factors to consider, and we still believe in the value of looking at historical pricing. What we do know when looking at Chart 1 is that we set a 17-year low for natural gas pricing in February 2016. We also made significant lows in the 12-month rolling forward for PJM/ComEd electricity around the same time (see chart 2). The question is if these lows are indicative of a defined bottom for these markets for the foreseeable future or whether this simply has been a bear market rally. The continued backwardation (prices lower the further out the curve) in both the natural gas and electricity forward curves could be interpreted as bearish. That said, from our position as risk managers for commercial energy accounts, we believe that it remains prudent to lock in at least half of a larger consumer’s obligation for a minimum period of three years. For smaller enterprises, we think that customers should look to lock their obligations for at least two years because the one factor (energy prices) that they can decide upon are at historically low levels. We acknowledge that prices can always go lower, but from a risk reward standpoint for consumers who have many other risk inputs, we think locking their energy risk is prudent.