Archive

For the last few years, both the domestic and international natural gas markets and their actual prices have focused on the abundant supply of natural gas provided by the drilling technique known as horizontal fracturing. In the opinion of some, this technique has many negative environmental characteristics (possible cause of earthquakes and polluted water tables among others), but it cannot be denied that this technique and the increased supply of low-priced produced product has transformed the natural gas business both domestically and internationally. The domestic result was a steady decline (with a couple of counter-trend rallies included) in prices from the July 2008 nearby Henry-Hub futures high of $13.38 per MMBtu to the March 2016 low of $1.71. As an example of international price moves, we would highlight that the Japanese Liquefied Natural Gas (LNG) Index has moved from a high of $18.11 per MMBtu in July 2012 to the most recent low of $5.86 Per MMBtu observed in May 2016.

There are no commodity markets that go straight up or down and the recent 73% rally in Henry Hub nearby futures from the aforementioned March 2016 $1.71 per MMBtu low to the $2.95 per MMBtu close for October 2016 futures can easily be understood to be a counter-trend rally. In fact, an observation of the backwardation (when prices are cheaper the further one goes out on the curve) of the current Henry Hub calendar strips would suggest that this will be a shortlived rally and that prices will be capped due to the overhang of supply that will return to the market if prices remain at these higher levels. It is important to note that this backwardation is significant. The price for the 2017 Henry Hub calendar strip closed September 30th at $3.13 per MMBtu, 9.58% higher than the 2019 Henry Hub calendar strip, which closed at $2.83 per MMBtu. While it is difficult to argue with the market, it is also important to examine the price drivers to see if there is some current mispricing and whether the backwardation is something that could disappear quickly even at these price levels.

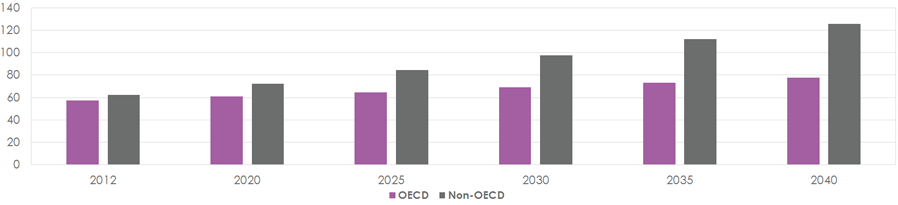

The important item in this article we would like to highlight is that there is a school of thought that believes there is a significant structural increase in natural gas demand starting to emerge. Some of the demand drivers are as follows. The Energy Information Administration (EIA) reported in its September 7th Short-Term Energy Outlook (STEO) that 2016 natural gas consumption for the electricity power sector (largest source of consumption) is going to rise 5.28% to 27.92 Billion Cubic Feet (BCF) per day from 2015 and will be 25.03% higher than the 22.33 BCF per day number in 2014. This seems poised to continue as natural gas-fired generation replaces retiring coal-fired electricity plants. Due to increased demand for natural gas for electricity production in newly deregulated Mexico, natural gas exports to Mexico could reach 3 BCF in 2016 and are expected to possibly reach 10 BCF in 2019 as it increases its pipeline capacity. Earlier this year, Cheniere began exporting LNG from their facility in Sabine Pass (Texas-Louisiana border) amid a global glut of global natural gas supply and tepid global demand. While there is concern over short-term global natural gas demand, an EIA study shows global demand growing quite nicely (see chart above) over the next 25 years. It could be argued that global demand for natural gas will increase more in both size and speed than currently projected as the world attempts to cut carbon emissions to reach targets agreed to by the signatories to the December 2015 Paris Climate agreement. While certainly still a fossil fuel, natural gas is cleaner on a relative basis and it can be argued that it will be used as the global “bridge” fossil fuel as the world continues to move away from petroleum and coal.

Analyst – David Mousseau

Information Sources – Energy Information Administration (EIA), CME, Reuters,Forbes and World Bank