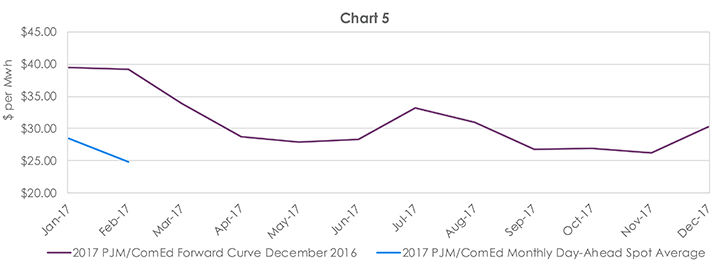

Charts 3 and 4 also show the extremely low spot prices that have occurred in calendar years 2015 and 2016. It is useful to observe that while the spot prices in 2015 exhibited the characteristics of a winter peaking market, the spot prices in 2016 were higher in the summer than the winter. While it can be argued that much of this is weather-related since the winter of 2015 was quite cold and the summer of 2016 warm, that may not be the most important takeaway. The natural gas market (usually the largest overall driver of electricity prices) rebounded from March to December 2016 and that explains much of the overperformance of spot prices in the second half of 2016 against the prices of the forward curve observed in December 2015. As we entered 2017, the forward curve in December 2016 implied a winter peaking market, mostly due to a fear of another type of polar vortex type of winter that was being forecast by some weather models that the energy industry pays attention to. As chart 5 shows, the actual spot prices in January and February were 32% lower than the forward curve predicted in late December 2016.

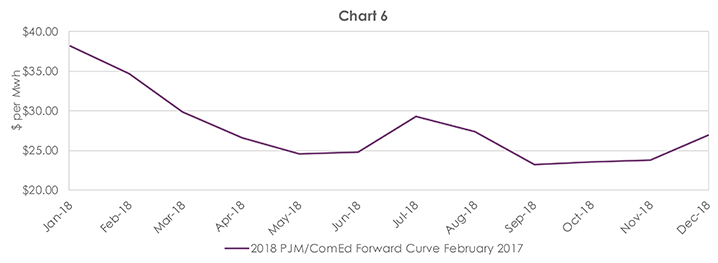

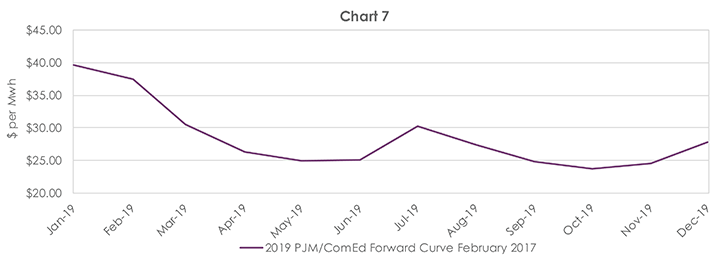

The forward curves in Chart 5, Chart 6, and Chart 7 all imply a winter peaking type market. The July and August prices for 2017, 2018, and 2019 average $29.73 per MWh while the observed average July and August prices for the years 2013-2016 were $31.38, bringing forth the conclusion that there is very little risk premium being attached to the summer prices for PJM/ComEd electricity pricing and that locking in prices for at least the summer portion of an electricity load is statistically a smart play. Alternatively, the average January and February price for 2018 and 2019 is $37.49, while the observed average prices for 2013-17 has been $37.89 per MWh. It is important to note that this observed data set includes the outlier pricing observed in January and February 2014, leading to the conclusion that January and February pricing for 2018 and 2019 has a fair amount of risk premium attached to it and that the actual prices have a good statistical chance of being lower. These are opportunities that should be considered by customers with the appropriate load shapes and sizes.

Analyst – David Mousseau

Information Sources – PJM, CME, and Reuters