During the second quarter, Frost and Sullivan (global market research and analysis company) released its Global Energy Storage Market Outlook 2018. The report finds that total installed energy storage capacity will grow 15.9% between 2017 and 2018 with the top six countries (China, USA, South Africa, Chile, France, and Israel) completing 1369 MWS of grid-scale energy storage system (ESS) projects during 2018. Continuing a recent trend, the costs of battery storage systems combined with concentrated utility-scale solar projects continue to fall to the point where they are becoming commercially competitive with traditional peaking power plants.

Since the impacts that energy storage can have on the current and future energy grid are substantial, we think it is important that our readers familiarize themselves a bit with energy storage technologies. Energy storage technologies are not new. While there is research occurring on many storage technologies, there are currently four types of energy storage technologies that can be considered deployed. They are Pumped Hydroelectric Storage (PHS), Compressed Air Storage (CAES), Advanced Battery Energy Storage (ABES), and Flywheel Energy Storage (FES).

The best known and most deployed technology is PHS, which accounts for about 93% of all United States energy storage. PHS systems generate electricity by pumping water from a low to a high reservoir during off-peak lower priced electricity periods and then releasing the water from the higher reservoir through a hydroelectric turbine when electricity demand is larger and prices are higher. In terms of future projects, the highest demand will be for ABES systems. At its core, an ABES systems will store electrical energy in the form of chemical energy that is then converted into electricity when needed. While ABES systems can provide the ability to store energy during low-priced periods and release electricity during periods of higher prices, one of the chief attractions of ABES is the ability to provide many other different grid services that are needed. These services include but are not limited to frequency regulation, voltage support, transmission congestion relief, and demand charge management.

One of the recent developments that highlights the importance of energy storage in the United States is the February 2018 Federal Energy Regulatory Commission (FERC) Order 841. This order finalized a rule designed to improve access for energy storage providers to participate in wholesale electricity markets. Specifically, the rule instructs the regional transmission operators (PJM, MISO, NY-ISO, etc.) to change their tariffs to “properly recognize” the physical and operational characteristics of electricity storage providers. The order specifies that electricity storage providers 1) be allowed to offer all the energy, capacity, and ancillary services that they can; 2) be dispatched by the regional transmission operators (RTOs); and 3) be capable of setting market clearing prices as both a buyer and seller. This rule will probably take 18 months to be approved and implemented, but it will accelerate a market that has been growing on its own.

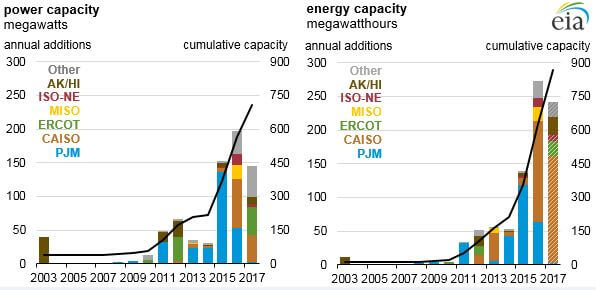

According to a May 2018 Energy Information Administration Report on USA Battery Energy Storage Market Trends, 708 megawatts of large-scale battery storage capacity were in operation at the end of 2017. Further, 80% of US large-scale battery storage capacity is provided by batteries based on lithium-ion chemistries, and 90% of battery storage projects were installed in regions covered by five of the seven organized independent system operators (ISOs) or in Alaska or Hawaii. Broken down further, 40% of the existing large-scale battery storage power capacity lies in the Pennsylvania-New Jersey-Maryland Interconnection (PJM), which is responsible for the energy and capacity markets and the transmission grid in 13 eastern states (including ComEd here in Illinois) and the District of Columbia.

It is important to point out that in 2012, PJM created a new frequency regulation market for fast-responding resources (which defines most battery energy storage projects). Initially, this provided a lucrative revenue source for battery energy storage systems, but the revenue has declined as there is a limited amount of frequency regulation required and there are many projects trying to provide the service. Part of the problem of energy storage integration into the wholesale power markets is best defined from the Executive Summary from the May 2018 EIA report: “Battery storage can serve many applications. However, the functional ability of storage to serve these applications has traditionally been not well defined under existing market rules and policies. As the technology has matured and the industry stakeholders in some regions have gained experience financing, procuring, and operating storage installations, the situation has changed and more clarity has begun to be provided. Most of the activity has been led by specific ISOs/RTOs and state-level regulators.” The important takeaway from this article is that FERC Order 841 is very important since the intellectual premise is that storage technologies are probably only going to get cheaper from a cost standpoint and will be part of the electricity industry landscape going forward.

Sources: Frost and Sullivan, Bloomberg, Federal Energy Regulation Commission (FERC), and Energy Information Administration (EIA)