It really was a surprise when at the end of the first day “No Press Conference Today” was announced. There was much conjecture beforehand, even that there would not be a deal, but it had to happen, with too much oil in the market and the price falling as OPEC wavered. In June they put 1mbpd in to the market and now they want it back.

The 175th Ordinary Meeting of the OPEC Conference

5 th OPEC and non-OPEC Ministerial meeting

Vienna, Austria, 6-7. December, 2018

OPEC & NON-OPEC HOLD TOGETHER & CUT BY 1.2MB

Yesterday, fraught with political and geo-political turmoil, they were unable to reach agreement. Today, with Russia and other non-OPEC members present, came the news that they have control and will cut by 1.2mbpd. No further information available but the market responded instantly moving up by 3% within minutes.

At the last meeting the cohesive feeling across the room with Saudi and Russia side by side and fellow members and non-OPEC producers supporting, it seemed that OPEC really was in control. That has since changed. Perhaps Saudi and Russia are just too close and with President Trump calling for more oil to reduce prices and Saudi giving it, who was running OPEC? Trump may need lower gasoline prices back home to keep the public happy and although they are not particularly interested in why the price of Gasoline moves, they just want it cheap and Trump wants to be the one to give it to them but why should OPEC comply?

In the few minutes yesterday in which we were allowed to join the Open Session, I spoke to Dr. Diamantino Pedro Azevedo, Minister from Angola and asked him what to expect. He felt that it would be good news, with OPEC united, looking for a price acceptable to both producers and consumers but wouldn’t indicate what that was! I mentioned that the price we had was close to the price that we had expected to see now, back in June. In terms of output he claimed to be at 1.5mbpd and could go higher. I suggested that the market had moved quickly upwards and back down again and he implied that was how investments moved.

In the few minutes yesterday in which we were allowed to join the Open Session, I spoke to Dr. Diamantino Pedro Azevedo, Minister from Angola and asked him what to expect. He felt that it would be good news, with OPEC united, looking for a price acceptable to both producers and consumers but wouldn’t indicate what that was! I mentioned that the price we had was close to the price that we had expected to see now, back in June. In terms of output he claimed to be at 1.5mbpd and could go higher. I suggested that the market had moved quickly upwards and back down again and he implied that was how investments moved.

I then moved on and spoke to Carlos Pérez the Minister from Ecuador. He said they were looking for an agreement to balance the market to bring down the excess in inventories. I asked if the cuts would be placed across all of OPEC members and he said that his point of view was that we should go back to the 2016 quotas and that would be discussed.

I then moved on and spoke to Carlos Pérez the Minister from Ecuador. He said they were looking for an agreement to balance the market to bring down the excess in inventories. I asked if the cuts would be placed across all of OPEC members and he said that his point of view was that we should go back to the 2016 quotas and that would be discussed.

I asked him how much of the decision making was down to members like him and how much to the Saudi-Russia combination. His response was that they all have equal voting rights but some of the larger producers have a political weight to consider and have different ideas. This remined me of schooldays, reading Orwell’s Animal Farm – “All animals are equal, some are more equal than others”. The members will vote and come to a decision but voting rights are not linked to output. Ecuador is currently producing 515,000 bpd but could go more, certainly up to his quota of 522,000 and the shortfall of 7,000b would be taken in to consideration when setting levels. Neither minister gave any hint of dissatisfaction over the Saudi-Russia, but any such dissent is probably not at their level.

From Iran came the view that Saudi created the problem and Saudi alone should deal with it and, amidst the conjecture, the announcement was made today that OPEC and its partners would cut output by 1mbpd. Now OPEC will not talk about price, the argument is based on the supply and demand figures available, most of them estimates as opposed to actual numbers.

Price is a most talked about number but not one that OPEC will adhere to. However, the probable range sought is likely to be in the $65 to $70 area, not too low but still appeasing President Trump and putting a cap on US Shale revenue too.

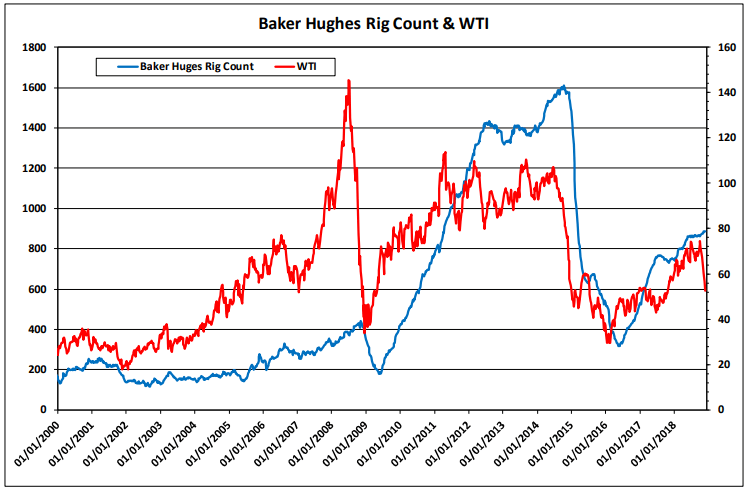

The higher prices in recent months have supported an increase in the US Rig count, as shown in the adjoining chart, illustrating the trend in both price and Rig count over eighteen years. With the market supposedly awash with oil, the US, having increased output by 2mbpd over the last year should share some of the credit for this and should be part of any balancing programme. That will not happen and for now, if there is to be any balancing, it will need to come from OPEC and its non-OPEC partners.

For OPEC, Supply Vs Demand is one of their favourite topics and such data is readily available from the US EIA, the OECD IEA and OPEC itself. Each provides similar data and may even collect from the same sources.

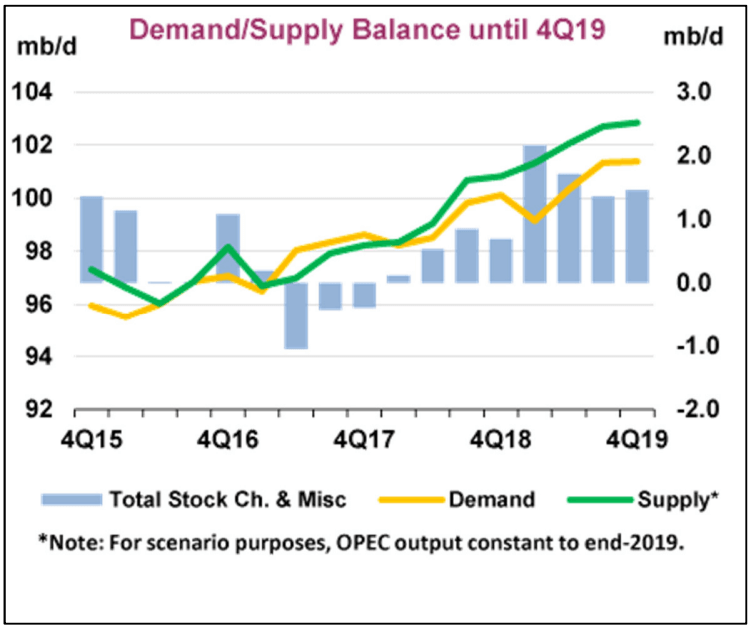

The adjoining chart from the IEA, clearly shows supply running ahead of demand with stocks building up having started the downward trend following the OPEC Meeting in June. The chart assumes OPEC output would remain constant but in light of the recent market collapse and subsequent outcome of this meeting, that will not now happen with OPEC announcing its cut to the market.

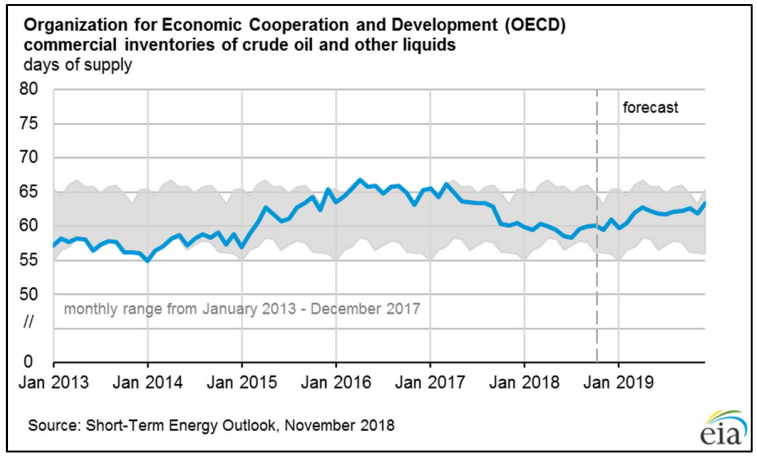

OECD stock levels have started to pick up again and this is another key indicator to OPEC and one reason why they originally decide to cut production to bring the levels down. But having increased output in recent months, they have allowed the levels to rise. Following the shortfall at the time of the meeting in June, when OPEC announced it would be increasing output, the market wasn’t convinced, and the price rose to $85. Then, once supply overtook demand, it fell back again as quickly as it had risen. Of course, whenever the price moves up rapidly, we hear the talk of $100 but many market followers seem to have short memories.

Not so long ago they were talking about $200 and then the market came down but as it started to rise earlier this year, there was talk again of the $100 level returning. What they fail to think about is that at that level, consumers cut back, conservation kicks in along with the revival of the US shale market and renewables. Conservation and the increased use of renewables will continue to rise and even more so as the price of oil passes the $75 mark and there is talk of the $100 level.

Market followers have recently spoken of the catastrophic collapse of the market with traders uncertain over which direction to go. If there is a chance that the market is going to change direction, they pile in and bet accordingly, without much regard for the consequences should the opportunity fail. The recent increases have been short lived and have not reached anywhere close to $100, so this collapse has been of far less significance than say that of 2014-5.

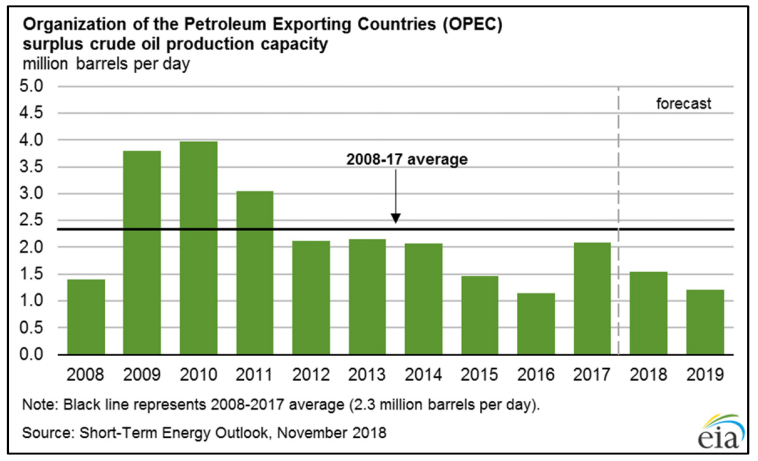

There is the balance between what output level OPEC can reach and what is left in reserve. Saudi has been pumping above 11mbpd in recent weeks to supposedly keep the price low and then when we look at what OPEC has in reserve, we can see from the attached chart that if a further need for more oil is required, OPEC won’t have much more than 1mbpd to spare. But as the US has increased output perhaps the US should share some responsibility for the collapse in the market.

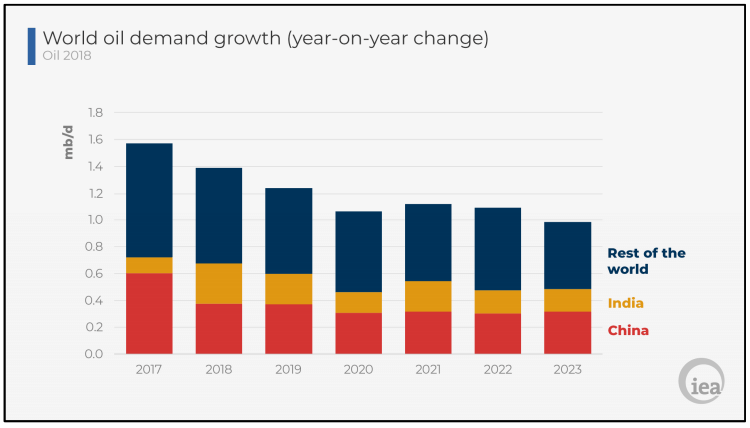

As of now, we are not entirely sure whether the market is going to pick up or falter. If the economies of China or the US falter, then the rest of the world will follow. Irrespective of this, when we look at the impact of numerous oil price shocks and climate change, the world is moving away from fossil fuels and embracing conservation as reflected in the adjoining chart from the IEA. It shows how the rate of demand for oil will continue to decrease year on year – sending another warning to OPEC and the global industry.

President Putin is happy to continue working with Saudi and OPEC and as a producer of 11mbpd he needs to be a party to any controls that are imposed to control the price of oil. That makes sense. The US has been supporting Saudi in its war against Iran in Yemen and also by the imposition of further sanctions against Iran, even though Iran is still a member of OPEC and still able to sell some of its oil while the US has deferred sanctions to some of its major customers.

Saudi needs US support anyway but its credibility has suffered seriously following the Khashoggi murder but with the initial support from Trump anyway, this has alleviated pressure from other countries even though they were astounded that it could have happened and that the President of the US could have brushed it aside so easily.

Therefore, Trump had the upper hand or rather did have, until the US Senate voted to cut or withdraw further support for Saudi in its war in Yemen. Then on Tuesday of this week, following a briefing of the Senate by the head of the CIA, Senators appeared convinced that the Crown Prince was personally responsible for the murder of Khashoggi. It is too soon to know what the outcome will be, between the US and Saudi, but there is certainly a split now between the Senate and the President over support for Saudi Arabia.

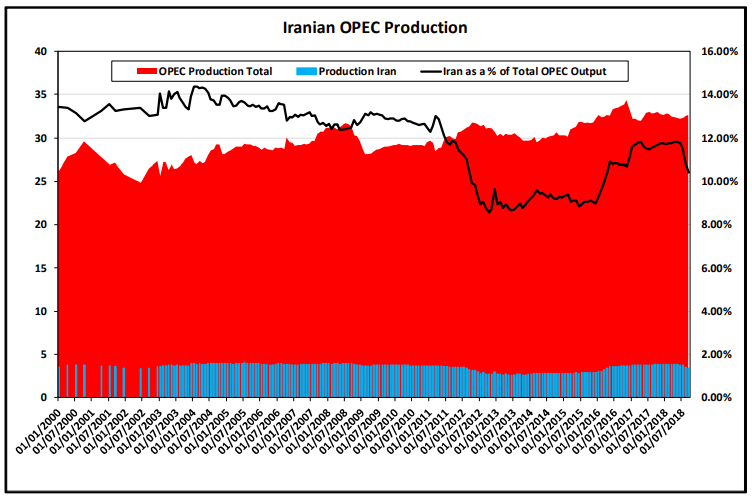

Something at least that will give some comfort to Iran, itself suffering partial sanctions at the whim of President Trump. Following the Nuclear Agreement in 2015, Iran had the opportunity to return to the world stage and increase its output by 2.5mbpd. The adjoining chart shows Iranian output and illustrates it as a percentage of total OPEC output showing clearly how it increased following the 2015 agreement and recently how it has since started to fall.

It is very difficult to know the precise reason why President Trump has announced he is pulling America out of the deal. It took two years to set up and the US was in it with other leading countries – UK, France, Germany, Russia and China – fully in agreement that Iran had met all directives. Even now, the other participants do not agree with the US and are keen to continue the deal. However, when Secretary Pompeo talks about Iran, he doesn’t actually refer to nuclear, but more about the Iranian support for terrorism. Of course, one also recognises that Iran and the US are on opposing sides in both Yemen and Syria, which may have a bearing.

President Rouhani of Iran is a moderate and worked hard to get the deal and has been keen to work with the West in terms of buying technology, goods and services. He has not had the support of the hard liners in the background and the Revolutionary Guard who are now using the threat of sanctions to build up anti-American and anti-Western sentiment. It is unlikely that Iran will back down, they have done all that was required of them to reach the nuclear deal and certainly will not agree to be a party to any cuts to their so-called quota within OPEC.

Rouhani is being pushed to respond and in retaliation has just renewed the threat to shut the Straits of Hormuz through which about one third of the world’s sea borne oil is shipped. In terms of the sanctions, whenever they are to be applied, Iran has the sympathy of the remaining four but that is all they can offer. President Trump has again repeated his call for “sanctions” but with Iran standing firm and not looking to back down, how far will America go, without starting another conflict in the Middle East.

The recent G-20 Meeting produced some interesting news clips and one of the best was the scene of President Putin and the Crown Price exchanging high fives like school kids, probably the two most despised people in there. President Trump was negotiating China, but on this occasion, he supposedly didn’t meet Putin following Russia’s act of aggression towards Ukraine.

In the time that the Crown Prince and Putin spent together they did agree that the Saudi-Russia co-operation would continue although, here again, details were not confirmed as to precise strategy to be adopted or discussed beforehand with OPEC members. At least agreement was made and whether the decision is taken to increase or decrease output, Russia will be an active party and without Russia and the token collection of other non-OPEC members, OPEC could well collapse. Russian co-operation is symbolic and it works for both sides. Meanwhile President Trump had, he claimed, stepped back from his trade war with China and reached a compromise that would, like the temporary deferring of the Iranian sanctions, diffuse some of the tension in the markets and furthermore, alleviate pressure on China and its economy.

Initially, markets responded positively but within hours realised that all they had to work on about the agreement, was a tweet from President Trump. Not even Trump’s key staff were able to explain what had been agreed and with Xi still away from home and not having fed information back, there was nothing apart from the tweet. Trump fired off another tweet identifying himself as the “Tariff Man”, panic set in and Wall Street collapsed by 3%.

The Chinese quickly responded positively but did not give out any detail and with the US market closed on Wednesday for the funeral of the late President Bush Senior, there was little reaction. However, since then, has come the news that the Chief Financial Officer of the Chinese company Huawei, who also happened to be the daughter of the founder, has been arrested in Canada, at the request of the US, seriously shaking the US-China accord while in the background there is some concern that the US and Chinese economies could weaken, impacting also on future oil demand.

The Dow fell a further 400 on this news alongside the falling oil price although much has since recovered. As a further side issue, North Korea seems to be expanding its long-range missile programme, putting in to question the US-North Korea relationship.

While Putin and the Crown Prince have their own way of dealing with enemies, either at home or elsewhere, President Trump will deal with his opponents by tweets. Yet, it is these three men, and not OPEC alone, who have the power to manipulate and control the oil price. With Russia on its side, supporting a joint strategy, Saudi Arabia can seemingly control the OPEC members but without Russia it will have no chance.

There are dissenters, such as Iran, suffering sanctions imposed by the US but alleviated to some extent by current wavers and support Russia. Iran will not accept any cuts at this time and others like Nigeria and Venezuela will be exempt. Libya meanwhile has returned with an output of almost 1.5mbpd but will also be exempt. Depending on how the relationship between the US and Saudi changes, Saudi could find itself increasingly isolated particularly in OPEC.

With OPEC output at a high point at 32.9mbpd and prices at lower levels, close to where OPEC had expected them to be at the time of the last meeting, the fall of around 30%would have had an impact on the US Shale market and this will have to be balance against lower oil/gasoline prices in the US. Admittedly the market is probably as comfortable now at $50 as it was five years ago at $100, having streamlined its operations and cut costs but not exempt from pain.

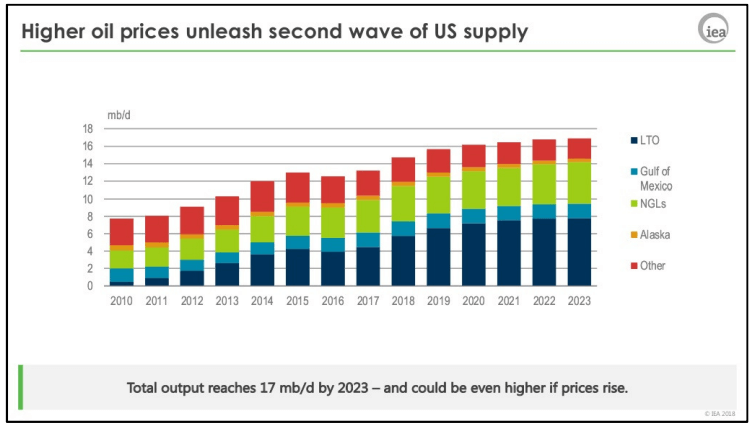

Looking at the chart above, it is interesting to see how US output is expected to move in line with oil price projections. OPEC has already unleashed the US market which has increased by around 2mbpd over the last year, also reducing its imports from 14mbpd to 2mbpd and looking ahead, is keen to increase exports to the rest of the World. The three main players today with around 11mbpd potential are Saudi, Russia and the US. Saudi is just one of three.

For now, the US supply is stifled by the lack of infrastructure, which hasn’t moved in line with the rig development although what is difficult in this respect is that rigs can be set up quickly while the infrastructure takes longer. There are of course plans to build or extend the existing pipe networking a release this oil on to the market. Moving north to Canada there are similar problems there where the infrastructure has also not kept pace with oil output.

Canada produces over 4mbpd of which 3mbpd goes to the US by rail and due to delays on various pipeline projects, no more can be moved. This is further exacerbated by the fact that Canadian production increases by around 300,000bpd each year and the only option now is to store or cut back on production.

Such news on its own sounds like Canada is following OPEC but the reality is that its oil is landlocked and has nowhere to go much like some US shale! Just long-term conservation.

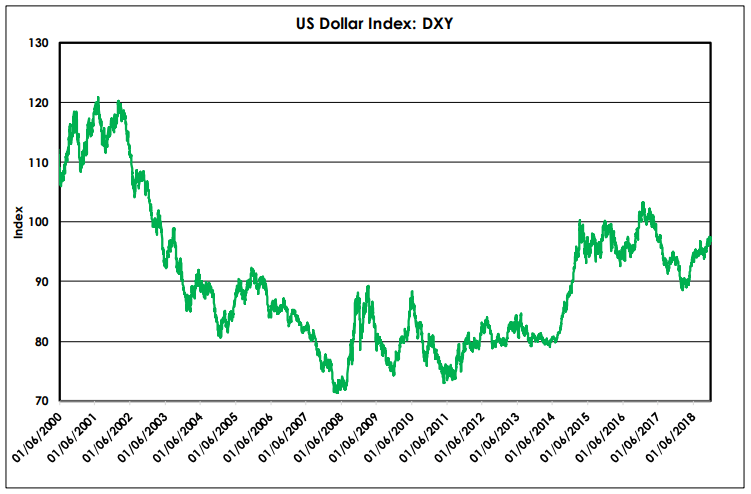

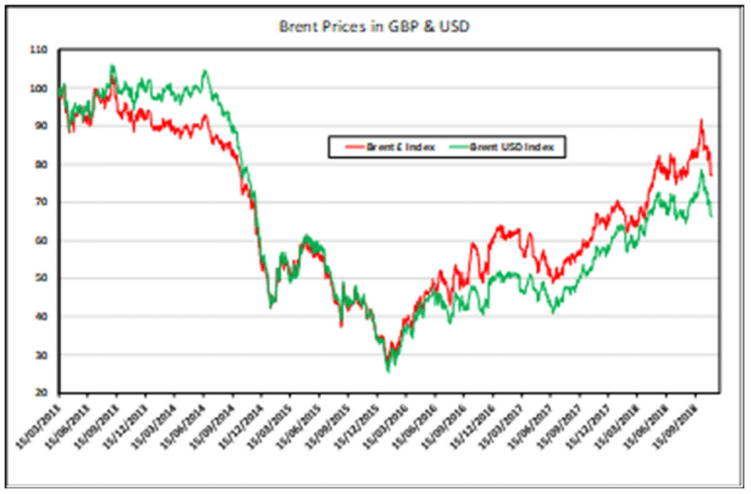

Oil is traded in the US Dollar For all producers, as the dollar fluctuates so too does their revenue and one can see from the chart above the dramatic fluctuation in the dollar against a range of currencies. Over the years there have been many plans to move trading through another currency and for countries like Russia and Iran, trading oil between themselves, there is a potential to do this. Unfortunately, all currencies fluctuate over time and one isn’t actually better than another.

The UK is one country particularly susceptible as it not only sells oil in dollars but also buys it in dollars and from the attached chart it has paid a higher price due to the continued weakness of sterling against the dollar.

Looking ahead, OPEC and its partners will have to decide whether the world economy will rise or fall and be prepared to move quickly whatever happens.

Within their own group they will also need to decide how they will continue to work with Russia and how far President Trump can or will support or push Saudi. It’s going to be a difficult time for them. And longer term, the difficulties will magnify.

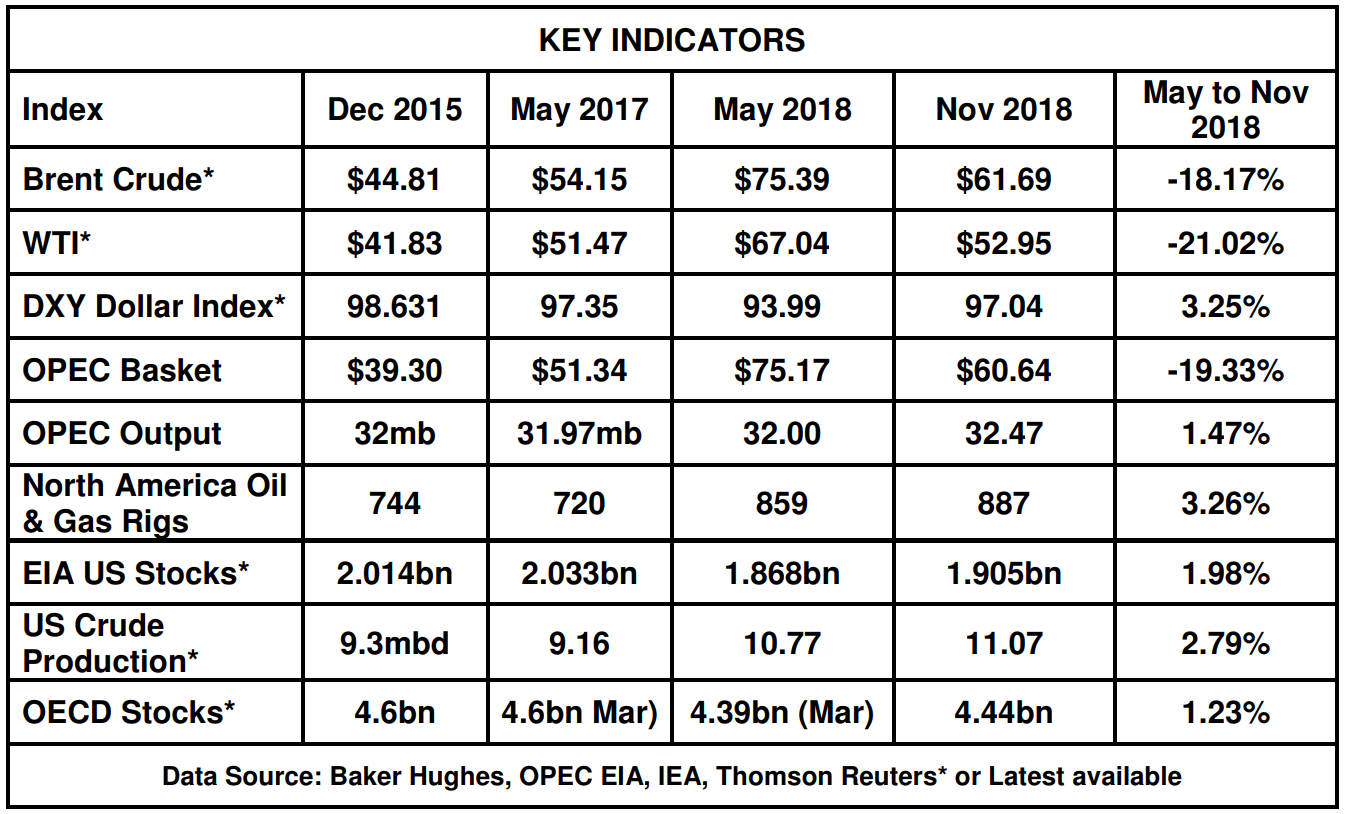

We have sets out below the key statistical pointers that have emerged from OPEC decisions in recent years and these are the factors that will determine their future success or failure.

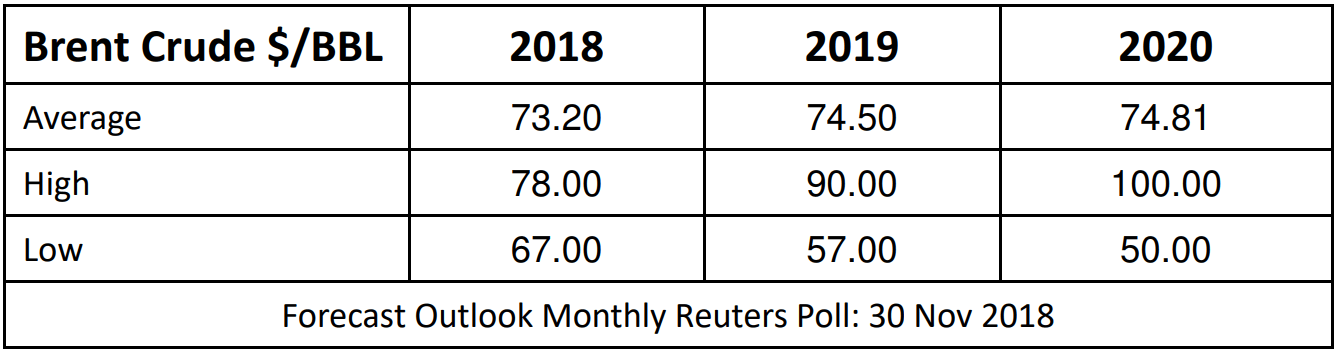

Forecasting the price of oil is almost a gamble. With Hedge Funds getting it wrong and investors backing the wrong direction it’s a precarious role. Ironically, looking at prices now, the original forecast that we set in June wasn’t too far out. For this one we have revised further.

As I have implied, looking ahead, there are many contentious issues to consider and as these are all in their infancy, it’s difficult to know what to expect. While writing this report events have moved on and I hope that at the point of issue it has been up to date across all topics but it’s simply a moving feast!

Iran is not going to sit back and wait to be told what to do, certainly not with the remaining four signatories to the 2015 deal giving support.