In 2018, the United States renewable energy market continued to grow despite a myriad of headwind issues such as federal tax reform, import tariffs, and a generally unfriendly federal political environment for renewables. The positive drivers of renewable energy growth are state and local policies advocating for the growth of renewables and establishing aggressive goals for renewable energy targets. Concurrent with the state and local policies is the record growth in corporate mandates to purchase renewable energy and to make commitments to achieve renewable targets. According to the Rocky Mountain Institute, corporate demand and actions added 6.43 GW of renewable generation, a 250% increase over 2017 growth rates.

Like both the electricity and natural gas markets in general, the renewable electricity market is regional in nature because many states have initiated their own renewable targets and subsidies in addition to federal tax credits. Further, some of the generation resides in regulated areas and other generation is in areas where their generators bid into a regional transmission organization (RTO) such as PJM, MISO etc. This leads to a renewable landscape that can be difficult to discern, and customers interested in renewables as part of their energy portfolio must try and understand the economics specific to them.

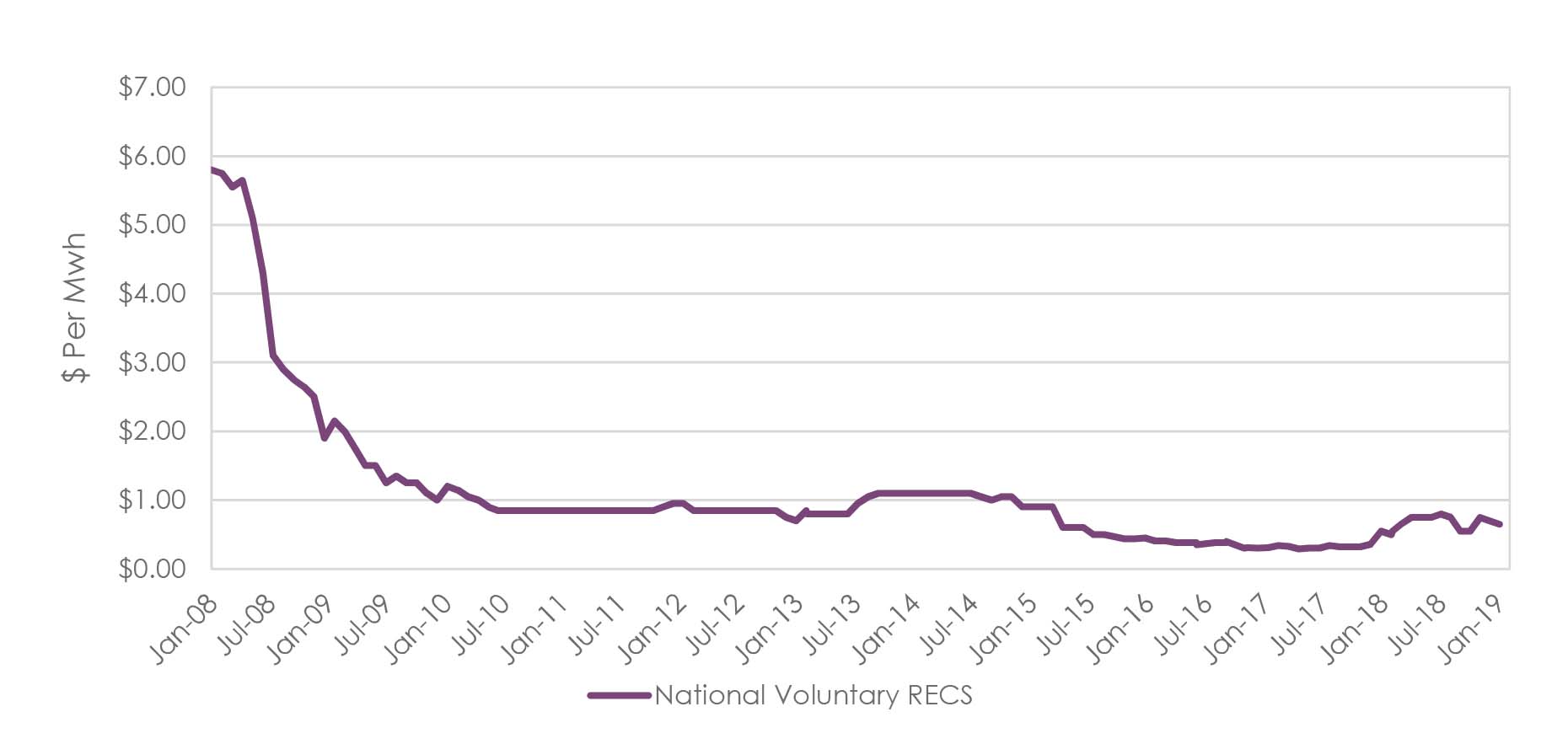

As referenced above, corporate demand for renewables has been increasing and evolving over the last few years. About 10 years ago, as the renewable market started to develop in earnest, corporate energy consumers started to purchase voluntary renewable energy credits (RECs) from renewable electricity generators. RECs are the environmental attributes separated from the actual electricity, allowing the corporate entities to claim that their electricity consumption was green regardless of where they were consuming it. The producers would then just sell their output into the wholesale electricity market or to utilities trying to reach renewable targets. The demand for voluntary RECs did not keep pace with the amount of renewable generation being built, and the prices for voluntary RECs declined rapidly with a low of around 30 cents per MWh hit in late 2017 before rebounding some in 2018 (see chart 1).

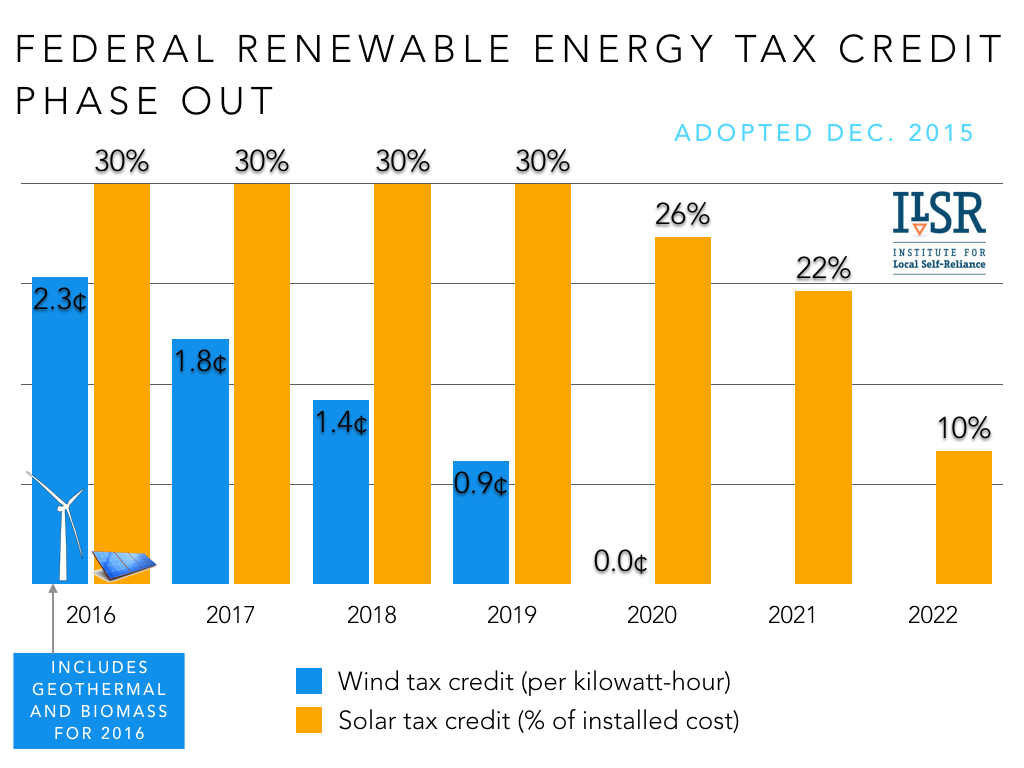

It is important to highlight that the primary driver in the proliferation of wind and solar electricity production facilities are the federal production tax credits. These credits are what generally allowed these facilities to be built. These separate production credits really caused a boom in the building of wind electricity farms in all parts of the country but concentrated in the Midwest and even more so in Texas. Corporate demand for renewable electricity has evolved, and recently the larger companies have either developed their own projects or have signed power purchasing agreements (PPAs) with project developers entitling them to a percentage of the output of a facility for a specified duration of time while providing for more flexibility.

Looking forward, the increasing desirability of corporations and their customers to support sustainability should provide the impetus for even higher demand for renewable energy. This is happening at a time when the Production Tax Credits (PTCs) are scheduled to be reduced or phased out completely over the next three years (See Table 1). Project developers have been trying to move forward projects so that they can still qualify for the credits, but again, the value of the credits is declining. There is always the possibility that the credits could be extended, but there is no assurance this is going to happen. At this point, wholesale electricity forward curves (especially in the Midwest) are not able to support the building of facilities without some sort of subsidy. So, we could be soon entering a period for renewable electricity where demand is increasing but supply is contracting, which will make the costs increase everything being equal.

For some clients (for example schools and property managers) who are not corporations that are thinking of greening their electricity supply, RECs are still cheap on a relative basis. An important aspect of RECs is that there is a registry that verifies that the green attributes you are purchasing have never been used even though the electricity has been produced. Each purchase of a REC helps reduce the backlog of RECs and will eventually cause an increase in prices that will allow for renewable generation to be built on its own. We point this out because if demand for voluntary RECs from the smaller participants in the market starts to increase, the price of the RECs could easily and quickly move out of the $.30-$1.00 per MWh range they have been trading in since 2010.

Sources: Energy Information Agency (EIA), Deloitte Consulting, ENEL