In these pages we, try to keep up to date with changes in the energy markets and their potential impact on prices and customers’ total energy spend. One area that has been growing is energy battery storage, and we would like to do a quick examination of that market, its potential impact on prices, and its longer-term viability.

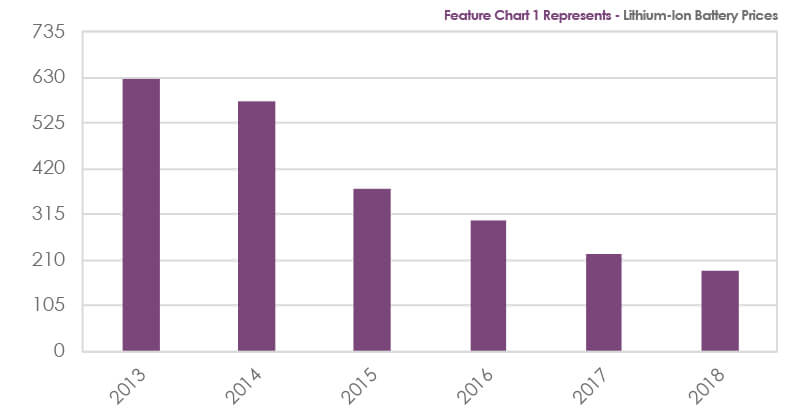

Energy battery storage is something that has been discussed for years, but this market has just started to grow since 2015. To be clear, energy battery storage allows an electricity generator to store electricity as it is generated to be deployed at another time. This could be a large natural gas generator or a commercial customer who has a small wind or solar project as part of its electricity mix. It must be pointed out that currently this is not a large part of the market. That said, it is one that has been growing dramatically, and there have been some large-scale utility storage projects that have been implemented and announced. There have been two primary drivers: 1. Battery prices that have been dropping dramatically, which has made utility-size storage projects almost competitive with natural gas peaking projects. 2. The ability to combine storage with intermittent renewable electricity generation. It is without a doubt that the extreme growth of renewable electricity generating projects (granted these have been subsidized with the costs appearing somewhere else) have contributed to the generally lower electricity prices that have been observed the last few years.

When looking at electricity storage economics, it is important to understand that the economics are not just about shifting power consumption from the pricier on-peak periods to cheaper off-peak periods. It is about the ability to deploy the storage at times of high demand, thereby reducing both capacity and monthly transmission distribution charges (usually determined by monthly high demand) that most electricity customers need to pay. This makes the economics quite micro if you will, dependent on the capacity and distribution costs in each Regional Transmission Organization (RTO) and utility area.

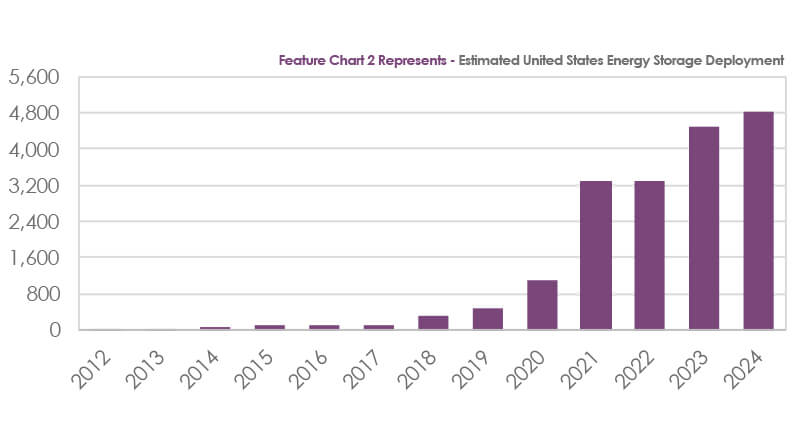

Woods Mackenzie just released their Q3 US Energy Storage Monitor. They highlighted that while 2nd quarter (quarter over quarter) deployments of storage projects had declined by 49%, year over year numbers for the 2nd quarter were up over 20%. More importantly, they project that the overall storage market will grow from 478 MWs estimated at the end of 2019 to 4834 MWs at the end of 2024, a 911% increase. In addition to the cheaper battery costs, policy support regarding storage in many individual states has been very strong as the states also understand that storage projects replacing peaking plants in areas of pipeline constraints (Massachusetts and NYC are good examples) makes sense from a policy perspective. It also helps individual utilities as the storage projects improve their ability to provide grid services as storage is an efficient way to provide frequency balancing (an essential grid service). In an example of the fact that the impact of storage and renewables is large, in the 2nd quarter, the Los Angeles Department of Water and Power announced a 300 MW/1200 MWh solar-paired storage project to replace a natural gas peaking plant.

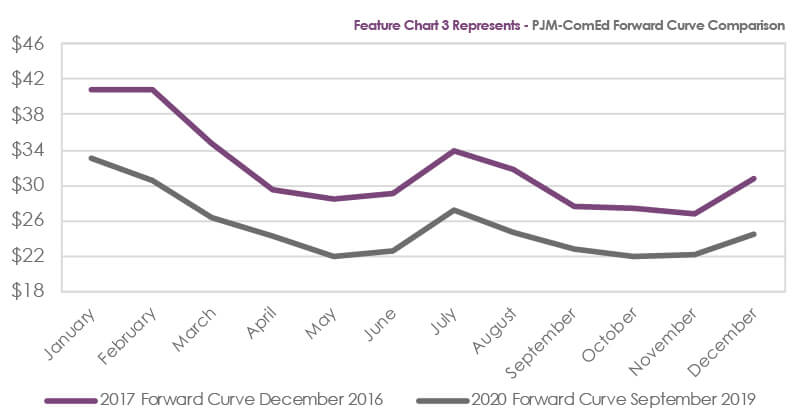

It can be difficult to gauge the impact of renewable electricity and storage on power pricing other than to say it has been bearish since all of the renewable projects are subsidized, so they tend to still produce electricity below their production costs (fixed costs-understanding that the marginal fuel (sun or wind) cost is not a factor). Keeping everything else equal, storage should have the impact of flattening the overall price curves since cheaper off-peak times will allow for increased demand to store the power and reduce the demand during the peak as the storage electricity is released. An examination of Chart 3 will show that forward price curves in general have been flattening, reducing the seasonality formally exhibited in the forward curves for PJM-ComEd power.

There are substantial costs involved installing renewable and storage projects. Additionally, the federal subsidies for both wind and solar are scheduled to decline or expire in the next few years. It is possible, however, that this could always be changed by Congress as the renewable electricity industry has become a powerful constituency. Employing renewable/storage projects is probably not for all customers, but for customers with bad load factors where electricity costs, especially demand-related charges, are a large component of their production costs, it may make sense to explore electricity storage options further. In any case, it does impact overall wholesale electricity prices, and we will keep our readers informed of developments in this space.

Sources: Utility Dive, Woods Mackenzie, and Bloomberg