After attending the 165th OPEC meeting in Vienna, John Hall, chairmain at alfaenergy, shares his thoughts on what was discussed.

Six months on after the last meeting and OPEC can still relax for a while longer as today the members announced that they would leave output levels as they were and review the position at their next meeting in December. Early indications were that there would not be any change but we all know that once in a while OPEC can surprise. However, this time members came late and left early.

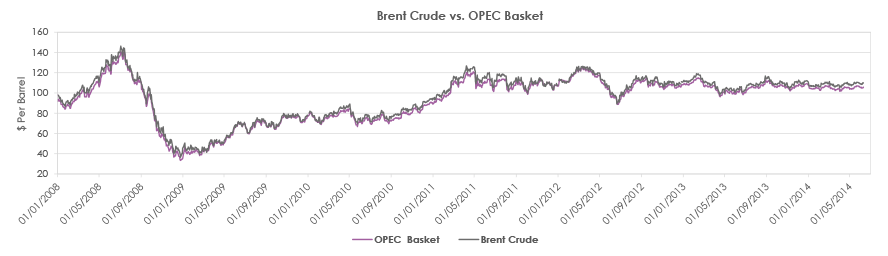

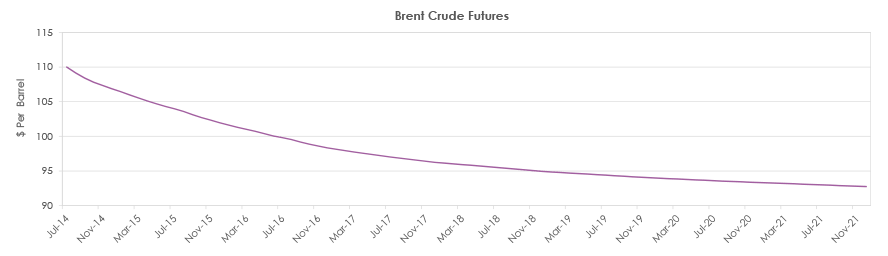

As we moved towards the meeting, the OPEC basket price maintained its level and rose slightly beforehand from $105.72 to $105.89 and for much of the year it has kept around this level. Yet contrary to expectations at the time of the last meeting, the price has remained over the $100 level for both the OPEC Basket and Brent Crude. It has not wavered by more than $5 as I indicated in my report then.

The OPEC President, HE Omar Ali El Shakmak, acting Minister of Oil and Gas of Libya, opened the proceedings by saying that there has been an upturn in the world economy although Russia, China and Brazil have not performed so well but overall economic growth is expected to increase to 3.4 per cent in 2014 from 2.9 per cent in 2013. As a consequence, OPEC expects world oil demand to grow by 1.1 mb/d to average 91.2 mb/d in 2014 with most of the growth coming from non-OECD countries. Turning to growth in non-OPEC oil supply, primarily North America and Brazil, he believes this will rise by 1.4 mb/d to reach 55.58 mb/d but conversely he is expecting output from Norway, the UK and Mexico to decline. OPEC is happy with the oil price ranging between $105 and $110, which it feels is fair to both producers and consumers, although if asked, consumers would expect the price to be closer to the $80-90 range. Taking all into account the conference confirmed that output will remain at 30mb/d.

However, behind the scenes geo-political tension and unrest in many of the producing countries has maintained pressure on the price and, in particular, because the so called come-backs from both Iran and Libya have not yet happened. In spite of hope that sanctions would be relaxed sufficiently for Iran to resume higher output levels and that the cessation of internal conflict in Libya would open up the oil flow again, neither has materialised.

Nevertheless Bijan Namdar Zangeneh, the Iranian Oil Minister, was very keen to say that he was ready to increase output by 700,000 bpd once sanctions were lifted. But we have to wait until then. Elsewhere the civil war continues in Syria and this is now spreading with renewed insurgency to Iraq following the taking of Mosul by an extremist group. While the lack of progress in Middle East peace activity will further impact the oil price, conversely, reduced tension between Ukraine and Russia has had a positive and moderating effect.

During the informal gathering with the various ministers, there was a very vocal outburst from a Nigerian protesting the presence and continued employment of Mrs Diezani Alison-Madueke, the Nigerian Oil Minister who has been accused of mismanaging finances both on a personal and corporate level. The protestor was ejected and the forum allowed to continue uninterrupted. General unrest in Nigeria and dissatisfaction over the performance of the President Goodluck Jonathan, who has been slow to respond to the kidnappings and atrocities committed by Boko Haram and continued support for his Oil Minister Mrs Diezani Alison-Madueke, can only hinder production and output of oil from a country rife with terrorism, poverty and corruption

I spoke to the ministers of both Angola and Kuwait and each seemed relaxed about prospects. Angola has aspirations to reach an output of 2 mbpd by next year and is actively seeking new markets in the east now that the US has reduced its requirement.

Meanwhile, OPEC spare capacity continues to wane and as domestic demand increases in all producing countries they are struggling to maintain and balance output between exports and domestic consumption. However, the real problem is that domestic consumption is highly subsidised and in some instances provided free so producers are presumably building the subsidies into the overall production cost and as the populations continue to increase so too will demand. Furthermore, in the aftermath of the initial “Arab Spring” it is unlikely that subsidies will be curtailed in the short term, if ever, and duty levels applied. I asked for clarification of this at the Press Conference and Mr El-Badri responded that all members are aware of the situation and trying to address it but as for the issue of “subsidies” this is one that cannot be touched and they will most certainly remain. I was surprisingly advised afterwards that this was not a subject for open discussion and was not a suitable question with which to open an OPEC Press Conference!

Looking ahead, OECD/US stocks will start to build up next month and the IEA has advised, closely in line with OPEC, that demand will increase this year by 1.32mbpd to 92.8mbpd. From the OPEC production tables in recent months it seems that most are producing as much as they can anyway and the real shortfall can be blamed on Libya which is now as low as 250,000 barrels per day, over 1m below its usual level, and with no clarity as to when that will improve.

So, once again, the support for increased crude will have to come from Saudi Arabia and I am confident that Saudi Arabia will discreetly increase production to cover any losses from the shortfalls of others and certainly with prices being maintained over the $100 level for the rest of the year.

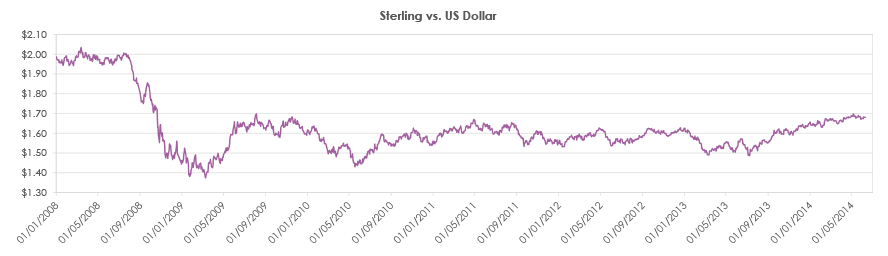

In the UK there has been some advantage by the higher exchange rate in recent months, filtering through to lower fuel prices while the balance between Petrol and Derv pricing has widened with diesel now being considerably more expensive than petrol by around 6ppl.

The wholesale price of each is similar, as is the duty, and I can only assume that as the car market is now changing back to petrol driven cars, with the advent of smaller high efficiency vehicles, the supermarkets who now control the market are using cheaper petrol as a marketing opportunity to entice customers into their stores and subsidising the discounts by applying a higher margin to diesel which tends to be used more by the commercial than the domestic market. The European refining balance is somewhat illogical with much of the Petrol that is produced being sent to the US while Diesel is imported from Russia.

The crude market is currently in backwardation and this will give support for stock building later in the year particularly by the US and other OECD countries. At the same time, US production will have increased and this will cause problems for both Canada and Mexico, two countries that traditionally supply the US with oil, and with the US moving closer to self-sufficiency their supply sources will no longer be so important and they will be forced to look for markets elsewhere. The US will continue to benefit shale gas, for as long as it remains cheap but once it exceeds the cost of coal, the US will switch away to using coal creating production blockages and increasing emissions.

Geo-political tension and the general supply demand scenario will continue to influence prices until the next meeting and beyond but I still do not expect to see any dramatic change in price. But by the time of the next meeting, OPEC will need to come back with a plan of action as to how to cope with rising external and internal demand.