It is the start of the year and we are dusting off our crystal ball. We will start with a look back at 2014 and move on to our predictions for 2015.

The past year has been an interesting one in terms of commodities. The price of oil collapsed nearly 50% from June, while gas has been over 30% and power over 20% since the start of the gas year in April. Renewables had a record high in UK power generation as cost of production collapsed for wind and solar manufacturers, making investments more economically viable. UK politicians kept out of the energy world this year, but it was a different story abroad with the Russian invasion of Ukraine. This not only affected the two countries involved, but the rest of Europe as well, highlighting how interconnected the market really is.

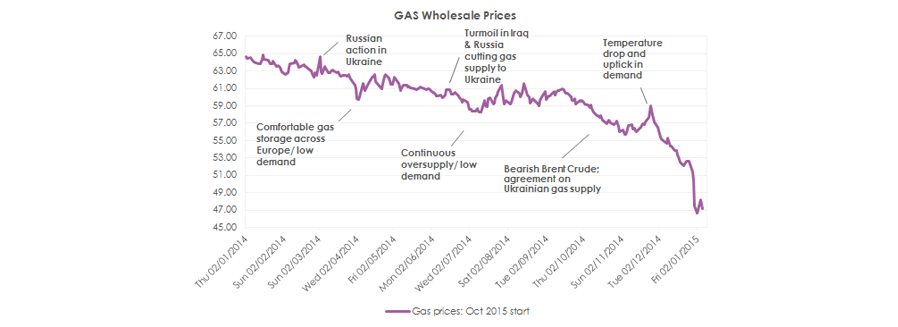

Gas prices in 2014 have been in a steady decline all year based on two fundamentals: high supply and decreasing demand. Supply into the UK has been strong, with no major disruption from imports in Norway and with the North Sea showing healthy flows all year. A strong and consistent supply of LNG all year helped start January with strong declines which followed throughout the year. With a strong supply system, storage levels continued to to be at the highest levels, continuing a four year streak.

Power prices were not as steep in their decline due to significant losses of generation capacity. Several nuclear power plants were offline due to leaks found in a number of cores. Gas fired generation was again not economical due to low spark spreads. Should demand have been higher there may not have been the declines as expected. Coal continued to play a dominant role in the supply mix, averaging 32% of supply for 2014 while gas and nuclear generation maintained around 20% of the supply mix, respectively.

Demand was consistently lower than expected, which in part can be attributed to the UK becoming more energy efficient as a whole. As energy costs rose, both domestic and commercial consumers were able to to look at reducing consumption in the form of more efficient boilers, solar panels for electricity and water heating, insulation of roofs, and better quality of new build. This all contributed in keeping demand down. In addition to this, a very mild winter at the start of the year and an almost non-existent one towards the end of the year added to the decrease in demand and prices for power and gas.

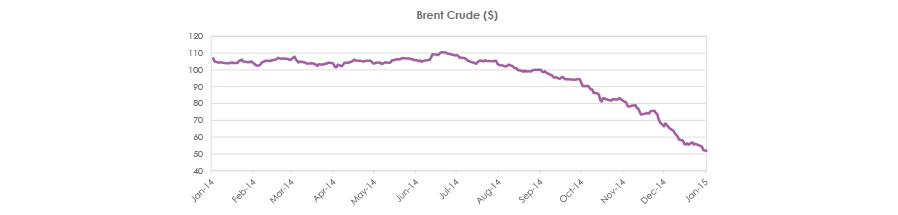

Oil prices were horizontal for much of the year until June 2014. Despite tension in the Middle East, the global demand for oil has been in decline all year. Furthermore, supply has risen exponentially due to increased US production where discoveries are now producing stable daily volumes. This, added to increase in supply from Libya and little to no disruptions in Iraq despite the ISIS threat, has meant that prices have only one way to go: down. Bad news for producers, good news for consumers and oil importing economies.

Renewables had a record high in supply generation. Average wind generation was up 1% in 2014 compared to 2013. Although wind is the dominant energy, other technologies are making significant headway. Solar, which was once too expensive, has become economically viable. Consumers who looked at it four years ago are now revisiting it as the paybacks are now within the investment criteria. Additionally, farmers are now exploring converting waste to energy or injecting gas to the grid as a means to create extra revenue for their businesses, going green in the process.

Ukraine has dominated the headlines for much of the year due to the Russian invasion. Europe’s vulnerability to Russian gas was first highlighted back in 2009 when Russia cut supplies to Ukraine over a pricing dispute. Europe was ill prepared then, but now it is ready in case gas taps end up being shut from Russia’s end. Gas storage facilities have improved, there has been an increase in gas connections, and a milder winter and lower demand have left the EU block in a far stronger position. To illustrate this, some countries currently hold over 90 days of supplies in storage. The diversification of EU gas supplies have also increased with LNG being the main new supply source from the likes of Qatar and soon the US.